The idiots behind the crime of the century

The LIBOR scandal edition

December 31st was an important date. No, I’m not talking about all the embarrassing crap you must you pulled while drunk. It marked the partial death of LIBOR, dubbed the world’s most important number.

You might not have heard of LIBOR but it’s deeply engrained in every part of our financial lives. Every time you use a credit card to buy the wrong sized underwear, take a loan to buy a house you can’t afford or buy penny stonks that have dollar debt, LIBOR is involved.

It’s tied to hundreds of trillions in notional financial contracts.

In this edition the mindstunninglyblowing story of LIBOR!

It’s the early 1940s, and the Second World War is raging across Europe. The Nazi’s occupy the Greek island of Crete. Minos Zombanakis, A whip-smart 17-year-old, escapes the Nazis to Athens, making a 200-mile journey in an open boat. He joins the University of Athens but quits later because he has no money. He stops a solder in the middle of a street and asks for a job. He finds work distributing aid with the British Army, the allies and the Greek central bank and the allies.

He later joins the Greek army to fight in the Korean War and returns to work with the Greek central bank. He's moved to Washington to oversee the implementation of the Marshall Plan to rebuild Europe. In Washington, he somehow convinces Harvard to let him join the postgraduate program despite the lack of qualifications and earns a masters in public administration.

In the 1950s, he joins Hanover Bank overseeing the Middle East. He becomes chaddi buddies with Khodadad Farmanfarmaian, Iran's central bank governor.

It’s the 1960s, and the Mohammad Reza Shah Pahlavi unleashes a series of dramatic economic reforms in Iran. There’s rapid industrialization and Iran’s economy is booming on the back of increasing oil revenues. But, inflation shoots up as the currency devalues and GDP starts to fall. The Shah isn’t bothered and pushes on with the next phase of economic reforms.

It’s 1969, and the Shah of Iran desperately needs some cash. Farmanfarmaian approaches his chaddi buddy Zombanakis for a loan of $80 million. It’s the 60-70s, fixed-rate loans are the norm and inflation in the UK is at 8% and rising. Minos knew that no single bank would take the risk of lending.

Minos assembles a syndicate of banks to lend. As for the lending rate, he comes up with an ingenious solution. Instead of a fixed rate, the interest rate would be reset every few months. Just before the reset, the banks in the syndicate would report their funding costs. The weighted average of the funding costs plus a spread would be the interest rate until the next reset. This is one of the first variable rate loans in history.

Minos names the rate the London Inter-Bank Offered Rate (LIBOR).

Sovereign syndicated loans explode, and later corporate loans as LIBOR is quickly adopted. LIBOR becomes even entrenched as London becomes the beating heart of the Eurodollar system—an offshore dollar-denominated financial system.

In 1984 UK banks ask the British Banker’s Association (BBA), a banking lobby group to create a standard benchmark for LIBOR. The BBA starts working with the Bank Of England and others and introduces an interest rate fixing mechanism for interest rate swaps in 1985 as a trial. In 1986, the BBA officially starts the current system of LIBOR fixing.

A series of geopolitical events, rising interest rates, inflation, and deregulation in the 80s-90s lead to the popularity of derivatives, interest rate and currency swaps. LIBOR, which is already popular, becomes the base rate for all these derivatives.

Over the years, LIBOR becomes embedded in every major financial instrument, from swaps, credit card rates to student loans.

Depending on estimates, $200-400 trillion worth of financial instruments is linked to LIBOR in some form or the other. That’s notional value and seems abnormally large, but that doesn’t mean the actual money riding on LIBOR is small by any measure.

LIBOR becomes the world’s most important number.

How does this LIEbor work?

You’d think that for such an important number, there would be a sophisticated methodology.

You’d be bloody wrong.

Here’s how LIBOR used to work, at least up until 2013-2014, when there was a small change. Every day around 11 AM London time, a group of banks submit a rate to the BBA at which they think they can borrow unsecured money from other banks. They submit a rate for seven maturities from overnight to 1 year in various currencies. The top 4 rates and bottom 4 rates are excluded to avoid outliers, and the average is the LIBOR rate.

The person submitting the rates to the BBA wasn't some high-level bank employee. Most often, it was a low-level junior clerk who got the rate by calling up a bunch of bank employees. The rate that moves trillions was essentially an opinion.

BBA: Hey Barclays, what’s your overnight LIBOR rate for the day?

Barclays: Wait, let me scientifically calculate it by asking our resident astrologer, Tarot card reading parrot and sticking a finger out to feel the wind!

Over time, India (MIBOR), Hong Kong (HIBOR), Singapore (SIBOR), Japan (TIBOR) created their own LIBOR style interbank offered rate (IBOR) benchmarks.

Pulling it out of your proverbial ass 🍑

People warned that there was scope for manipulating LIBOR as far back as 1991 & 1996, but nobody cared. Surprisingly, shockingly, it turns out LIBOR was being manipulated.

Cue the surprise! 😲

Calls and emails in 2007 warned Fed officials that the LIBOR fixing was actually being fixed.

“Fix”, what a delightfully ironic term 😂

The global financial crisis was raging in 2008, and banks across the US and Europe were facing significant liquidity crunches. The largest banks in the world were insolvent.

Banks have regulatory liquidity requirements and liquidity needs. Suppose there’s a mismatch on a day-to-day basis, they borrow from other banks to balance their books—this is called the interbank lending market. Pre-2008, this was a deep and liquid market with 100s of billion in volumes.

But in 2008, pretty much all banks were insolvent, and there was significant stress in the interbank markets. They were selectively frozen even in some cases. What most people don’t know is the Federal Reserve’s intervened indirectly in the money markets at a scale never seen in history. The Fed backstopped the entire global financial system by activating swap lines with major central banks and providing unprecedented levels of dollar liquidity. Adam Tooze wrote about this brilliantly in his magisterial book Crashed.

Now, remember LIBOR is the rate at which banks think that they can borrow from other banks—not actual borrowing. So, theoretically, banks that were finding it hard to borrow money in 2008 would report higher LIBOR rates because nobody was lending to them and rates would go up.

It turns out that wasn’t the case.

Several major banks like Barclays and RBS outright lied by reporting artificially low LIBOR rates. Since LIBOR was unsecured, it gave an indication of the credit quality of banks and at the depths of 2008, every bank was royally buggered 🎍. The interbank and money markets were frozen, banks weren't able to borrow at any rate.

Reporting the actual LIBOR rates would’ve meant even more pressure on stock prices and potential bank runs.

There were a series of revelations throughout 2008 that everybody from traders, bank CEOs to central bank officials like Timothy Geithner of the US Treasury and Mervyn King, head of the Bank Of England, knew that banks were pulling LIBOR out of their asses. In 2017 BBC aired a recording that showed the Bank of England pressuring British banks to report lower LIBOR rates.

Several investigations led to fines of over $9 billion against Barclays, UBS, RBS, JP Morgan, Citibank, among others.

The ghosts of 2008 past

After 2008, the unsecured interbank lending market pretty much disappeared. From billions, the daily volumes shrunk to a few hundred million. Banks needed an existential threat to figure out that unsecured lending was risky.

In all fairness, there was no possible way for the banks to know that unsecured lending was risky. I mean who could’ve guessed lending without collateral was risky? Not me!

The regulators also tightened the screws by increasing the reserve requirements for unsecured lending, which made it even unattractive.

Following the LIBOR scandal, Martin Wheatley of the UK Financial Services Authority (FSA) submitted a report on how to reform LIBOR. Two key recommendations were:

1. Find someone new to administer LIBOR instead of the BBA

2. Use actual transaction data in determining LIBOR.

In 2014, the Intercontinental Exchange Benchmark Administration (IBA) took over the administration of LIBOR.

But here’s the sad news, by 2013-2014, unsecured interbank volumes had almost totally dried up. There weren't enough transactions to determine the LIBOR rate 😂. Over the years, it got really bad and given that there were no transactions, LIBOR was based on “expert judgement”, in other words, still made up.

How LIBOR was Determined👇

So the paradox of Libor is that if we are looking for a robust way to create transparency on bank funding costs, Libor is not that rate. Because the market it measures is a small to disappearing part of overall bank funding, it can no longer claim to accurately reflect the marginal cost of funds for banks, nor to provide end users with confidence their interest payments are directly linked to those costs.

— Andrew Bailey, Governor of the Bank of England

Make me happy, honey…

While lying about LIBOR during the 2008 crisis was one side of the story, there’s a whole other side. Derivates were the biggest financial instrument tied to the LIBOR. Everything from plain vanilla forwards, futures to exotic swaps—$200 trillion of notional value.

LIBOR is a short term rate and doesn't move much on a daily basis. So, even a 1 basis point (0.01%) move can mean a lot of money given the leveraged derivative bets on its direction.

Banks were the biggest traders of Eurodollar futures tied to the LIBOR rates. Given that LIBOR wasn't a market-determined rate but the “opinion” of banks, it was rife for abuse.

You know what happened next?

It was abused.

Cue surprise, shock, and horror 😱🙀

Now, it’s important to understand the incentives at play here. Banks have large trading desks that bet house money. Traders make more money in bonuses if they make money for the banks. So, everybody had an incentive to manipulate LIBOR. It’s unclear when—It could've been as far back as the early 90s, but bank traders trading Eurodollar futures started manipulating LIBOR.

Now, you’d think that there would be some sophisticated and deeply secretive scheme to manipulate LIBOR. After all, it was an important rate with hundreds of trillions of derivatives betting on it.

But the way LIBOR was manipulated was comical, to say the least. It's like the script of parody movie.

Traders were openly talking about moving it up or down on Bloomberg chat rooms, emails, and phone calls that they knew were being recorded.

I mean, my nephew uses Signal messenger to threaten his classmates!

In 2013, The Commodity Futures Trading Commission (CFTC) fined Royal Bank of Scotland (RBS) $325 million for manipulating LIBOR. In the press release, it released select transcripts of messages from traders and boy, oh boy, was it funny. Here are a few gems💎:

August 20, 2007

Yen Trader 4: where’s young [Yen Trader 1] thinking of setting it?

Yen Trader 1: where would you like it[,] libor that is[,] same as yesterday is call

Yen Trader 4: haha, glad you clarified ! mixed feelings but mostly I’d like it all lower so the world starts to make a little more sense.

Senior Yen Trader: the whole HF [hedge fund] world will be kissing you instead of calling me if libor move lower

Yen Trader 1: ok, i will move the curve down[,] 1bp[,] maybe more[,] if I can

August 20, 2007

Bank A Trader: im puzzled as to why 3m libor fixing not coming off after the FED action

Bank B Trader: [UBS] is lending dolls through my currencies in 3 month do u see him doing the same in urs

Senior Yen Trader: yes[,] he always led usd in my mkt[,] the jpy libor is a cartel now

Senior Yen Trader: its just amazing how libor fixing can make you that much money

Senior Yen Trader: its a cartel now in london[.] they smack all the 1yr irs ..and fix it very high or low

September 3, 2009

Senior Yen Trader: [Yen Trader 6], can you ask [Primary Submitter] to drop 3m Libor by 1 bps? hold 6m libor unchange [sic] thanks

Yen Trader 6: Yes going over to his desk now[,] yup, 6s going unch, 3s will drop by 1

Senior Yen Trader: domo

From a CFTC order against UBS:

November 8, 2006: Senior Yen Trader: "have put some pressure on a few people i know to get libors up today, mailnly 6m as i am paid that one, let me know if that doesn't suit or if there are any particularly you need up .... only did a few lyr trades, wish i'd done a lot more now!"

January 19, 2007

Senior Yen Trader: "hi [ ... ] , bit cheeky but if you know who sets your libors and you aren't the other way I have some absolutely massive 3m fixes the next few days and would really appreciate a high 3m fix, [Yen Bank C] were one of the lowest y/day at .51. Anytime i can return the favour let me know as the guys here are pretty accomodating to me ... "

Yen Banl( C Trader: "I will try my best, but really fed up with my guys, wanted a high 6m yesterday, but came in really low (our guys one of the main culprits)-got quite badly hit on that"

Senior Yen Trader: "you and me both, you need 6m high? if so will get my guys to set high for you today, yesterday they set 3m up at 57 for me!"

June 25, 2009

Euro Trader-Submitter 1: "u need low 3s and/or 6s? we need low 6s ... boys, we send the fixings in about 1hr, so let us know pls"

Euro Trader 1: "low 6s high 12s please" Euro Trader-Submitter 1: "noted" Rates Manager A: "JUST BE CAREFUL DUDE"

Euro Trader-Submitter 1: "yeah [Sterling Trader-Submitter 1] gave me ur call update i agree we shouldnt ve been talking about putting fixings for our positions on public chat just wanted to get some transparency though otherwise we end up with the same talks afterwards why we fixed it low or high, from u boysinldn"

From an FCA notice against Barclays

Firm A said “[Firm B] u ask for 75” (i.e. a fix rate of 75) and Barclays added “we delivered…but i dont wanna kiss from u…i just take a beer”.

Tom Hayes was a gifted trader and a mathematician with Asperger's. He became the first trader to be jailed in the LIBOR scandal. If I’m not wrong, the only one. What made Tom different was that he was doing what everybody was doing, but he took it to the extreme and was labelled the “ringleader” of the scandal.

Most securities regulators and authorities only go after cases they know they can win for sure. For a variety of reasons, from incompetence to lack of budgets, white-collar crime prosecutions have fallen around the world. On a side note, this is the story of Jesse Eisinger's must-read book The Chickenshit Club. Unfortunately for Tom Hayes, he was a sure thing and became the fall guy.

What made Tom different as Liam Vaughan and Gavin Finch wrote in The Fix is that he understood the role brokers played in fixing LIBOR. Reports and transcripts in the aftermath of the scandal, snowed that the brokers had significant influence over LIBOR fixing through their relationships with bank employees.

Tom was a genius trader and was generating humongous volumes. Naturally, the brokers and Tom became tight chaddi buddies.

His messages are on a whole new level:

By the time the market opened in London, Lehman’s demise was official. Hayes instant-messaged one of his trusted brokers in the U.K. capital to tell him what direction he wanted Libor to move. Typically, he skipped any pleasantries. “Cash mate, really need it lower,” Hayes typed. “What’s the score?”

From this Guardian profile:

For the umpteenth time since Lehman faltered, Hayes reached out to his brokers in London. “I need you to keep it as low as possible, all right?” he told one of them in a message. “I’ll pay you, you know, $50,000, $100,000, whatever. Whatever you want, all right?”

“All right,” the broker repeated.

“I’m a man of my word,” Hayes said.

“I know you are. No, that’s done, right, leave it to me,” the broker said.

Talking to UBS trader and a broker:

If you keep 6s [i.e., the six-month JPY Libor rate] unchanged today … I will f—ing do one humongous deal with you … Like a 50,000 buck deal, whatever … I need you to keep it as low as possible … if you do that …. I'll pay you, you know, 50,000 dollars, 100,000 dollars… whatever you want … I'm a man of my word.

We are talking about bloody LIBOR—a bloody rate that’s deeply embedded in modern finance. The LIBOR scandal was called the crime of the century and it was perpetrated by a bunch of absolutely gifted morons!

These idiots were talking about moving it as if they were ordering shawarma rolls on Zomato!

I mean, come on!

I am sympathetic toward hardworking income redistributors (scamsters), but this is insulting to honest scamsters.

No bank CEOs or higher-ups went to jail. There were even widespread allegations that Bob Damond, the former CEO of Barclays knew about the LIBOR manipulation.

But it was just some lowly trader who was jailed.

This is why I keep saying, financial scams are the easiest way to make money. You have to be a real fucking idiot to get caught. As long as you use common sense, you can make 100 times the money you’d make by working in a 9-6 job like a moron!

Curtains down

December 31st, 2021, marked the beginning of the end for LIBOR.

The FCA announced that all Swiss franc and euro LIBOR settings, the 1 Week and 2 Month U.S. dollar LIBOR settings, and the Overnight/Spot Next, 1 Week, 2-Month and 12-Month sterling and Japanese yen LIBOR settings will cease immediately after December 31, 2021, and that the Overnight and 12-Month U.S. dollar LIBOR settings will cease immediately after June 30, 2023. - ICE

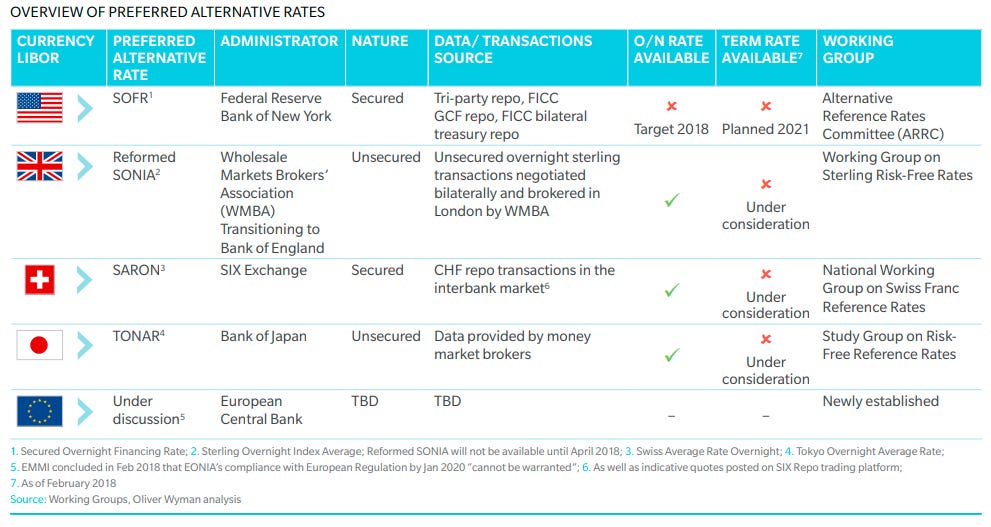

Central banks worldwide have already chosen rates like the Secured Overnight Financing Rate (SOFR) as replacements, but there are teething troubles.

The most popular replacements, such as the SOFR, are based on secured overnight rates. Meaning they don’t have a credit component embedded in the rate. So SOFR behaves differently than LIBOR, and you could see that during COVID when the spreads widened significantly. There's still some debate over this though.

The other issue is that these are overnight rates, and there’s no term structure, unlike LIBOR, which has maturities from overnight to one year. This has led to a debate over whether rates like SOFR and SONIA are suitable replacements for LIBOR.

Few things on my reading list. These LIBOR and banking industry shenanigans are quite fascinating.

The Fix: How Bankers Lied, Cheated and Colluded to Rig the World's Most Important Number

The Chickenshit Club: Why the Justice Department Fails to Prosecute Executives

Crashed: How a Decade of Financial Crises Changed the World. I’ve read this book, and I highly recommend it.

What the hell is this Eurodolalr system Jeff Snider, Snider series.

Good reads

Should Passive Investors Be Happy Buying Equities at 100x Earnings?

There are always two sides to every investment: The number and the story.

Goldman Sachs destroys one of the most persistent myths about investing in stocks 🤯

'Long' Factors, not 'Short' Change : Long Only Factor Portfolios in India

What happens when the frenzy ends and the world doesn’t value your valuables?

Is monetary policy still able to influence growth?

Codetermination: the missing alternative in corporate governance