Like a drunk guy singing a rap song

The Tipsheet

Top of the news

Pay for investments, stay for the entertainment

Everything is content, as the brilliant Ranjan Roy wrote on the Margins recently. What do you think the primary job of an asset manager or a wealth manager is? To manage money for the investors, right? What if that’s not the case? What if asset managers, wealth managers, advisors, etc are really content marketers managing assets on the side? A second priority if you will.

Sounds a bit preposterous, isn’t it? But it’s kinda true if you think about it. These asset managers and wealth managers spend more time on publishing content than they do on asset management. The financial services industry is probably the biggest producer of content on the planet. And they do a horrible job of it and most of it is pure garbage. The Indian firms are especially worse. Their content strategies are as coherent as a drunk guy singing a rap song, but that’s a separate argument.

"To the window, to the wall!" Drunk Guy On The Subway

These guys publish all sorts of content like market outlooks, trade ideas, economic analyses, stock & fund recommendations, and so on. But what exactly is this content? Is it advice or just analysis? Well, according to Jimmy Cayne, the former CEO of Bear Stearns, it’s entertainment.

Here’s a ridiculous story of a client who sued Bear after lost millions trading currencies on the advice of Wayne Angell, the chief economist at Bear. And this was the defense of Bear in the case. And shockingly, they won.

Economists, Cayne testified, “don’t really have a good record as far as predicting the future.” Shockingly, he added, “I think that it is entertainment, but [Angell] probably doesn’t think it is.” I doubt that the Count was entertained or amused. Cayne even noted that Angell did not have a real job description at Bear. “I don’t know how he spends most of his time,” testified Cayne. “He travels a lot and visits people and has lunches and dinners and he is an entertainer.”

So the next time you listen to your broker, AMC, wealth manager, etc, remember, they are entertaining you with their gyan. It’s not advice.

Impersonal finances

Nothing scares and confuses investors like asset allocation. In fact, this has to be the most common question people ask. Asset allocation at its core is assembling different asset classes that move differently. I think one of the reasons why asset allocation tends to intimidate people is because everybody keeps saying the same goddamn thing – “asset allocation is the most important thing that determines your returns” or some variant of it without any context. It has to be among the most annoying things in finance.

But if you strip away all the nonsense and go the basics, things become a whole lot clearer. Here are two really telling excerpts from this piece by Anish on this:

If you don’t know where you are going, any road will get you there. So, the first question one must answer is: what are the goals one is saving and investing for? From there flows most of the solutions.

Bogle clarifies in Common Sense on Mutual Funds that, initially, he also misunderstood the study. Further, he goes on to say that there is no formula for deciding one’s asset allocation, and he in his retired life went with a 50:50 allocation to equity and bonds. It all depends on your goals, risk ability, and tolerance.

Continuing on the same vein, why is all this stuff about investing, personal finance so complex? Blame the goddamn salesmen. If everybody from asset managers to advisors made things really uncomplicated, why would you even need them? Most of these hucksters are only in business because they make up all sorts of horseshit to sell their overpriced useless funds and services. Here’s a brilliant post that will most likely make you feel like shit because you probably deserve to.

At its core, this stuff is pretty simple. However, the business of religion and the business of personal finance are a lot like the business of golf instruction. They tend to deliberately overcomplicate things. People want Answers. The more confused people are about what they’re trying to accomplish, and how they might accomplish it, the more money there is to be made selling Answers. Maybe that’s a gap wedge with a diamond dusted face. Maybe it’s healing crystals. Maybe it’s rental real estate.

Marxists are ruining the markets

“Sensational bullshit can travel around the world and back again while nuance is lacing up its boots.”. This is one of those cases. In 2016, Sanford Bernstein published a paper salaciously titled “The Silent Road to Serfdom: Why Passive Investing is Worse Than Marxism,”. For context, Bernstein offers a bouquet of actively managed funds, many of them which have refused to beat their benchmarks. Apparently, they can beat the benchmarks, but they are refusing to do so on principle, protesting the Marxist invasion of low-cost index funds. This stupid excuse for an opinion piece was debunked by a lot of people but looks like it’s back again.

Annie Lowrey decided to resurrect the piece in The Atlantic and goes on a rant about a bunch of things like concentration, common ownership, collusion, and so on. Leave it to the smart people on Twitter to point out the stupidity.

My thoughts on this piece:

1) Article says indexers control corp America, but are inactive on corp actions. Huh?

2) Passive needs active to work. See "myth of passive investing".

3) @CliffordAsness destroyed the "Marxist" piece 5 years ago. https://t.co/NoVPBH4giZ https://t.co/1tsIhpGnZD

Would you like to own some people?

If you’re bullish on a company, the easiest way to play that is to buy a stock. But what if you’re bullish on some person but he doesn’t have a company? This is a bit tough because SEBI doesn’t yet allow humans to be listed on the stock exchanges and you can’t really buy that person. That is unless that person agrees to be sold to you OTC, but that opens a whole new can of worms. For example, what if that person underperforms? You can’t sell the person, liquidity is an issue, how will you charge the fees?

Enter Bitclout, which is solving the problem of betting on people without actually having to own the underlying people. BitClout is a decentralized social network platform like Twitter. Everybody that signups on the platform gets a creator coin that can be traded like a stock.

In the long run BitClout would like to be not just a complement to Twitter where you can speculate on creators’ success, but an actual substitute. Except instead of all the money going to the platform in the form of ad revenue, creators would have a crypto-native way to monetize. They could offer exclusive content and priority access to token-holders, and similar to NFTs, fans could signal to creators that they really believe in them by buying a bunch of tokens—much more effective than just replying to all their tweets!

But the platform is in the news for all sorts of bad reasons. But nonetheless, this is quite fascinating. A lot of garbage comes from the crypto world, but once in a while something mildly sensible…ish too.

Archego…ing still

The exact details of the Archegos saga might never become public. But thanks to the fiasco, there’s been some really good reporting and writing on the broader world of family offices, investment banks, and other intermediaries. This week FT published a long read on family offices.

Over 7000 family office with over $5.9 trillion in assets

Average assets of $1.9 billion

Family offices are so lightly regulated that the head of the CFTC estimated that the cost of their regulatory disclosures was just $28.50

The fallout from the blowout is becoming apparent. Credit Suisse revealed that it will take a $4.7bn hit from the episode. It also fired over 7 people including the chief risk and compliance officers. But here’s the funny part, they apparently had an award for risk management in February

Timing of these #CreditSuisse awards seem amusing 😂 https://t.co/HdCmtGo4pq

A unique take on the potential fallout from any possible regulations of prime brokers:

In general it’s good to assume that when banks take on too much risk & get burned, exchanges win. It happened in 2008 when banks were forced to de-leverage & let exchanges electronify dealer-owned markets, and it might happen again today. Since their inception, clearinghouses like those owned by ICE & CME have not experienced a default, and continue to serve as a viable solution for OTC markets gone wrong. If regulators do make changes to existing market structure as a result of the Archegos supernova, I suspect it will put even more power in the hands of exchanges & data providers who already control a large amount of market influence today.

A gaggle of links

Investing & Personal finance

No Moat is Safe and Moats are for never

Why You Shouldn’t Pick Individual Stocks

SIP vs Lump sum: Which is a better way to invest in mutual funds?

Do older investors earn higher returns than younger investors?

The Changing Nature of Momentum

Why Portfolio Diversification Still Works

Should you Buy and Hold in Emerging Markets?

Vanguard Mishap Leads to an Estimated $200 Million Windfall for Investors

2020’s Big Market Moves Catch Most Active Funds Flat-Footed

Death to the Lost Decade. In Search of a More Balanced Approach to Asset Allocation

Economy

What 100 contracts reveal about China’s development lending

What democratization of finance sounds like on Clubhouse

Tech & Internet

The cesspool of the internet is to be found in a village in North Holland

Why Sahil Lavingia is betting his company on the rise of the creator economy

Don’t pick up! The rise and fall of a massive industry based on missed calls

Startup, VCs, and other creatures

April 6, 2021 How much is Basecamp worth? I don’t know and I don’t care.

Global Venture Funding Hits All-Time Record High $125B In Q1 2021

Crypto

‘Silent crash’ as price floors collapse across NFT space

Welcome to Decentraland, where NFTs meet a virtual world

Research

Retail Financial Innovation and Stock Market Dynamics: The Case of Target Date Funds

The Public Health Effects of Legalizing Marijuana

Visuals

I guess time will tell if gold is broken, or if it’s merely catching its breath. Either way, you can’t help but notice how unusual this recent decline is given the fact that gold didn’t work when everything said that it should.

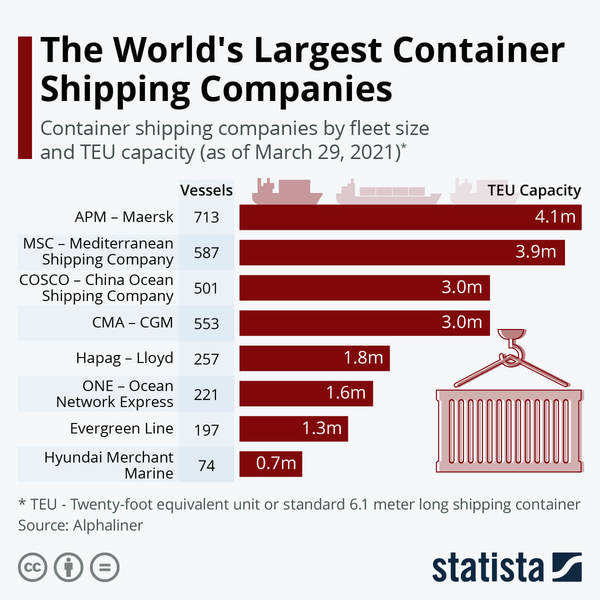

It’s just astounding how big these shipping companies are.

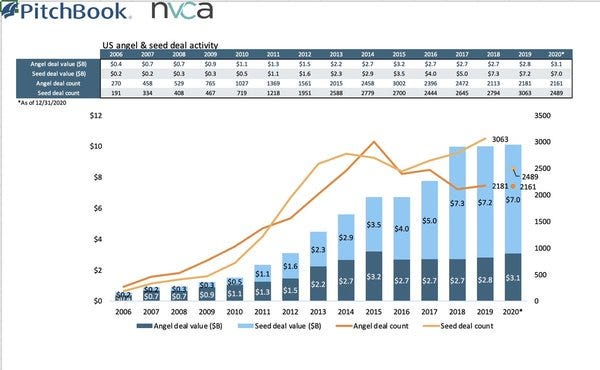

It’s raining money. Never been a better time to be a startup.

Videos

https://www.youtube.com/watch?v=mayqIvr50dE

Hester Pierce, one of the SEC commissioners on a Bitcoin ETF

Hester ETF CLIP

The opening of this conversation was stuck in my mind. It’s so true, isn’t it?

“Good afternoon everybody we got Ted Sarandos randos here from Netflix though otherwise known as my drug dealer.”

Ted Sarandos Interviewed by Jason Hirschhorn | Upfront Summit 2020

Tweets

Public blockchains will be the title registries for everything of value.

Ultimately, NFTs will authenticate the world.**

There are many arguments in and about tech, some better than others, but the idea that tech startup creation has declined is hard to describe as anything other than a deliberate lie. https://t.co/cUjHRatEFo

Unofficial list of the 16 greatest investments ever

(Minimum gain of $1B) 🧵

1/ The best of the best

◻️Naspers - Tencent (2001): $32m -> $250B (7800x)

◻️Softbank - Alibaba (2000): $20m -> $100B (5000x)

“Skin in the game” as a risk management tool is the same as saying you should not be afraid to ride in a car with a drunk or stoned driver because he would be putting his own life at risk by not driving safely.

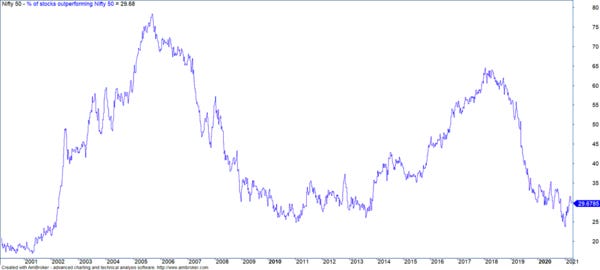

Percentage of Stocks that beat Nifty Returns over a 10 year period https://t.co/xrCXjL7pj6

If you don't want these updates anymore, please unsubscribe here.

If you were forwarded this newsletter and you like it, you can subscribe here.

Created with Revue by Twitter