How to run a successful Ponzi scheme

The Tipsheet

It’s was a ridiculous week littered with unicorns, decacorns, popcorn, and all sorts of other ridiculously unbelievable things. This environment feels like it’s straight out of a parody movie. But angina aside, it’s fun living through a phase when we keep hitting fresh new highs on the “no this isn’t real, it’s a dream, slap me and wake me up” index.

Here’s this week’s edition of links and other damn things. If you enjoy reading this do share it with your friends who are aspiring Ponzi schemers.

Top of the news

A step by step guide to a successful investment scam

This was a sad week for all aspiring scamsters. The Shah Rukh Khan of financial scams, Bernie Madoff, passed away this week. He ran one of the largest and most successful Ponzi schemes in history. His scam spanned 136 countries, and he defrauded over 37,000 people to the tune of $65 billion dollars. Bernie was a legend, I’ll miss you, Bernie. I have a lot of sympathy for people who want to run investing scams. It’s harder than ever to run an honest scam thanks to the internet and the general evolution of the capital markets, and it’s tough to hide things. You can run scams, but it’s very, very hard to run long scams and the odds of you getting caught within five years are higher.

But, how do you run a successful investing? It’s not really complicated as long as you need to get these 6 basic steps right:

A really good story

A killer strategy name and a brilliant presentation. Something like a Quantum Artificial Intelligence Behavioral Market Neutral Double Delta Momentum Arbitrage strategy. Promise triple the market returns with half the volatility

A really good and believable presentation. Can’t stress this enough

Sales guys fluent in bullshit

A YES, NO sales strategy. Initially, you gotta work hard to attract suckers. But once you reach a certain size, you have to stop. After this, you have to start saying no to everyone, which will bring more people. The more you say no, the smarter the people you’ll attract which will be good for your credibility

Take money from new investors, take a small cut, and give the rest to the old investors

Keep doing this

That’s it. It’s that easy. But the reason why a lot of talented and promising Ponzi schemers get caught is that they take the presentation part for granted. They tend to have images like this one used by Bernie:

Lembas

Sure, this will look good for the people who are dummies. But the smart people won’t buy this, and they end up looking closely, write articles, file complaints with the regulators and you don’t want that. The key is to make that line look slightly volatile. throw in a few down months here and there. A group of quantitative Ponzi schemers actually did some research which found that making the returns line volatile by 10% increased the Ponzi scheme’s success rates by at least 15%.

So the lesson from the Bernie Madoff scheme is to not commit fraud. It’s to focus on the presentation, they can make or break your Ponzi scheme. It’s all about the presentation, presentation, presentation.

But joking aside, the scale and duration of the scam is stunning. Goes to show how destructive greed can be. A few good reads on the scam:

An interview of Harry Markopolos who had been warning the SEC of the scam for decades but wasn’t taken seriously:

In finance there is a term, the Sharpe Ratio, which is a measure of how many units of return you earn for each unit of risk you take. Madoff’s Sharpe Ratio was off the charts over a decade-and-a-half time period, ranging between 2.5 to 4.0 for most time frames. Sharpe Ratios this high have existed for shorter time periods but never for 15 years in a row – no one is that good! But investors wanted to believe in the Holy Grail so they suspended their disbelief and acted like moths before a flame

A piece by Ed Thorp who figured out the scam as far back as 1991 when he was hired by a firm to conduct due diligence:

In my attempt, via “networking,” to find out how much other money was invested with Madoff I repeatedly heard that all his investors were told not to disclose their relationship, even to each other, on threat of being dropped. I was able to “locate” about half a billion and inferred that the scheme had to be much larger. I was given one investor’s track record, showing steady monthly gains in the 20% annualized range back to 1979, and was told the record was similar back into the late 1960s. It appeared as though the scheme had already been operating for more than twenty years!

Surprising things

There were some crazy, surprising things about this sordid mess. Did you know Bernie Madoff invented the concept of payment for order flow? Bernie, though a scammer was quite tech-savvy.

Most people focus on the Ponzi scheme, but before his downfall Bernie Madoff was an influential part of the exchange industry.

Every exchange has a run-in with Madoff at important times in their history - here's how: https://t.co/Y4fGYfQS7x

Another surprising albeit funny thing I came across was that JP Morgan, Madoff’s bank of choice, knew that he was a fraud all along and was even short on Madoff thorough structured notes

The best one is that the deceased Libyan dictator Moammar Gadhafi turned down a chance to invest with Bernie. A bloody dictator had more sense than the smartest hedge funds.

Oh and Helaine Olen, the author of “Pound Foolish: Exposing the Dark Side of the Personal Finance Industry” has an interesting theory about Bernie and the popularity of index funds:

I’ve long been convinced that there is a link between the end of Madoff’s scheme and the overwhelming popularity of index-fund investing in the aftermath of the financial crisis. It’s not simply that, as the Wall Street Journal theorized, people realized pricey money managers hadn’t seen what was coming.

Instead, Madoff demonstrated the lie that almost any savvy individual investor could produce steady gains in a way that nothing else could. By destroying the retirements and dreams of so many, he inadvertently performed a much-needed service.

In a case that has riveted Singapore’s moneyed-classes, Ng was charged last month with four counts of fraud for allegedly raising at least S$1 billion (US$740 million) from investors for commodity trades that didn’t exist. Much about Ng and his dealings remains shrouded in mystery. But open court proceedings, interviews with investors and charge sheets by Singapore prosecutors indicate the young financier was able to raise huge sums of money by touting average quarterly gains of 15%.

Unicorns or farting donkeys?

What?

It’s raining unicorns in India and Tiger Global is the new unicorn-maker. We’re just four months into 2020, and Tiger is responsible for six unicorns. And it looks like it’s not yet done:

Tiger Global has finalized — or is in late stages of concluding — more than 25 deals with Indian startups this year. About 10 of those investments have been unveiled so far while the rest, ranging from $10 million dollars to over $100 million, are in the pipeline for the coming weeks and months.

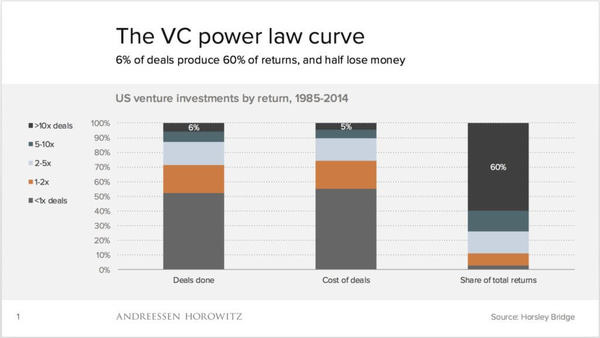

Venture capital is just like music, movies, or investing in stocks. A small number of hits tend to deliver all the gains. Take a look at the numbers

Who?

So, if this is the case, how do you make money? By investing in as many companies as possible. But then, there are too many venture capital firms with too much money chasing the same set of companies. Which begs two questions. Where is all this money coming from and how do you compete in this environment?

Where’s the money coming from? Well, the dominant narrative is that there’s too much liquidity, and it’s true. But people attribute this liquidity to central bank money printing, which I don’t fully agree with, but that’s a discussion for another day. But, a lot of entities like pensions, endowments, family offices, etc do have a lot of money to invest. And pensions have return targets because they have to match the liabilities of the pension participants and pay them over a period of time. And the problem with pensions is that they are massively underfunded. Given the near ZERO bond yields, they need alternatives. And hence PE/VC allocations have hit new highs.

Even though a lot of research shows that PE/VC returns have been abysmal, it hasn’t stopped these pools of money from allocating more to them.

How?

So how do you compete if there’s too much money chasing too few deals? By forgetting what the words “due-diligence” and “valuations” mean and partying like it’s the 90s. Here’s a brilliant piece by Everett Randle on how Tiger is rewriting the VC playbook by throwing all notions of what’s right in the dustbin:

The hedge fund most often in the crosshairs is Tiger Global — a tech-focused “crossover” that has dominated media headlines & VC gossip circles for the last 12 months due to its record-breaking deal pace & aggressive style. From an outsider’s perspective, Tiger’s investment strategy can be roughly summed up as:

* Be (very) aggressive in pre-empting good tech businesses

* Move (very) quickly through diligence & term sheet issuance

* Pay (very) high prices relative to historical norms and/or competitors

* Take a (very) lightweight approach to company involvement post-investment

* Above all, deploy capital, deploy capital, deploy capital

So?

But the downside of playing fast and loose is that startups will take advantage of the lack of due diligence. Here’s an excerpt from an ET piece:

A freshly minted unicorn got in trouble with its brand new investor, among the most aggressive VC shops in the world. The company in a recent announcement boasted about the number of users that had signed on to its platform. Everyone lapped up the news, but for the money bags, who were fuming, we hear. Their peeve: They were sold a different number all together and they bought that hook, line and sinker. Turns out the difference in the number of users shown to the press and the investors was almost 7 million.

If unicorns are companies with $1 billion valuations, I dub companies who sell bullshit stories to get unicorn valuations as farting donkeys. And I have a feeling that a lot of unicorns will turn out to be farting donkeys.

At this stage in this upside world, we live in, it’s time to re-read the story of Theranos, one of the greatest venture capital cons of all time:

How did Theranos become a $9 billion company? Elizabeth told a great story. She was able to sell the idea that if everyone helped her, if everyone invested in her idea, they could be part of something big. They could save people. Together, they would change the world. And that’s how the big con begins: creating a good story. A story that people want to share, that people want to be part of. We all want to make a difference in the world and make it a better place. Perhaps Elizabeth Holmes did, too… Until it interfered with her own goals, one of which was to become the next Steve Jobs.

It’s madness just how crazy the funding environment is. I remember seeing a joke on Twitter when went something like “If you accidentally walk into a VC’s office, you might come out as a Unicorn”. This is a golden age to raise money for ideas and companies that will never make money and are allergic to sustainable business models.

Some crazy stories:

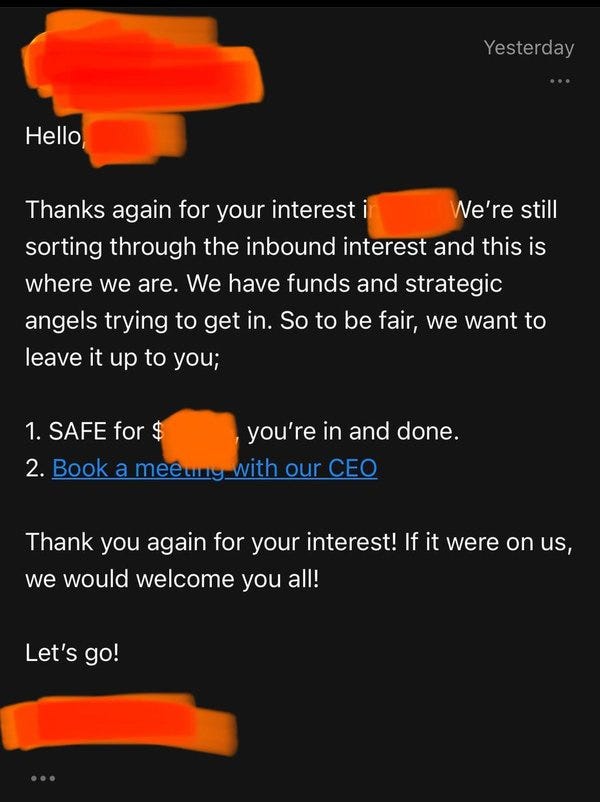

The atmosphere of sheer panic among VCs these days is disconcerting. If I was an LP, I would be sitting on my hands right now. Up and down the capital stack, people have lost their wits, if not their minds.

A VC fund partner DM’d me this note that they got from a YC founder - basically “thanks for your interest, here are the docs to sign, no need to meet with the founders”

The attached docs are at a $100M price 😂 https://t.co/YCj3A90a6L

Enough and more being said about the liquidity in the market. It’s raining capital across stages for startups in India. How are investors and startups likely to respond? Some thoughts below 👇

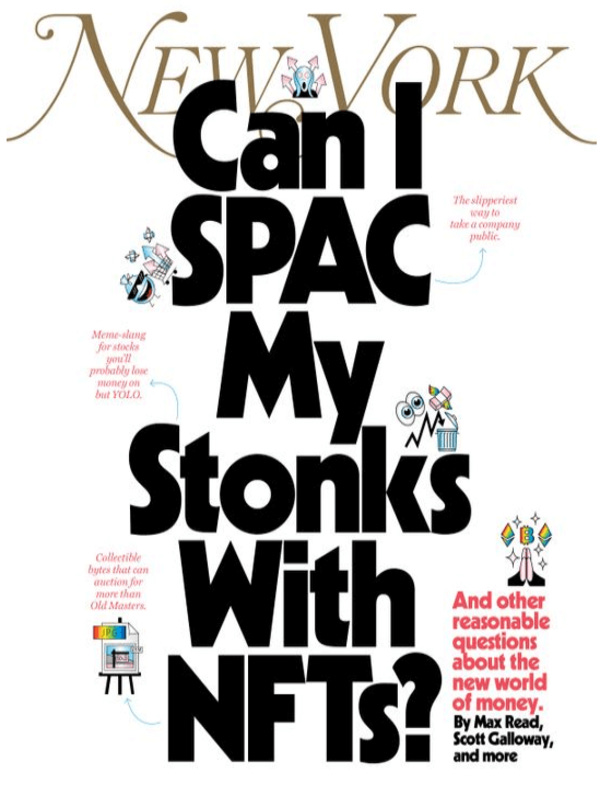

The magazine cover indicator

There’s this well-known theory in the market circles that whenever a famous magazine cover makes a bold prediction, you should do the opposite. As funny as it sounds, there’s some truth to it:

In 2016, Gregory Marks and Brent Donnelly of Citigroup looked at The Economist and “selected 44 cover images from between 1998 and 2016 that seemed to make an optimistic or pessimistic point.” They found that impactful covers with a strong visual bias tended to be contrarian 68% of the time after 1 year.[5] The latest example of this phenomenon being The Economist’s Living in a low rate world[6] from September 2016, weeks before one of the fastest selloffs in global fixed income.

Here’s the New York Magazine cover this week.

And it looks like the Magazine Cover Indicator might still hold true. People shorting SPACs have been increasing off late. And NFT prices are down by nearly 70% from their peak.

A gaggle of links

Investing & Personal finance

The Most Important Rule in Investing

The Delusions of Crowds: Why People Go Mad in Groups

“In a way, bubble investors can be thought of as capitalism’s unwitting philanthropists.”

Active Equity: “Reports of My Death Are Greatly Exaggerated”

Confessions of an Overnight Millionaire “I constantly ask myself, Do I deserve this money?”

There’s Nothing to Do Except Gamble

Asset Allocation Is A Strategy For Capturing Average Results – Part 1 & Part 2

The case for private equity at Vanguard

How to Avoid Falling Victim to the Next Madoff

The Dark Side of Thematic Funds. Funds with compelling stories don’t always make sound investments.

A place for Indians to discuss and evaluate Investments • r/IndiaInvestments

A place to discuss investments, insurance, finance, economy, and markets in India.

Markets

What an 18th-Century Stock Market Bubble Can Teach Us About the SPAC Frenzy

The Explosion of SPACs — Should You Care?

The College Friends Who Bet Their Way to Billions

Economy

Tech

What 250 Years of Innovation History Reveals About Our Green Future

Email from Jeff Bezos to employees

Cloudflare’s Intelligent Design

Startups, VCs, Fintech and other creatures

Is Strategic Money an Oxymoron?

The Third Wave of Online Education

Nubank: The World’s Biggest Digital Bank

Crypto

A crypto wonk is running the SEC

Miscellaneous oddities

The story of pro wrestling in the twentieth century is the story of American capitalism.

If You Want to Make It As a Writer, For God’s Sakes, Be Weird

Playlist

Joe Weisenthal - Rapid Fire (EP.42) - Infinite Loops | Podcast on Spotify

Listen to this episode from Infinite Loops on Spotify. In this episode of Infinite Loops, we spoke with Joe Weisenthal, Executive Editor of Digital News at Bloomberg. In this fun and thought-provoking conversation we chat: • NFTs • Bitcoin Believers and its viability • MMT • Robinhood • And MANY more sensitive subjects Follow Joe on Twitter (Twitter.com/thestalwart).

#398: Web Smith on The Future of Media - The Pomp Podcast | Podcast on Spotify

Listen to this episode from The Pomp Podcast on Spotify. Web Smith is the Founder of 2PM, an unique company that creates some of the best reports and summaries breaking down the DTC industry. In this conversation, we discuss the future of media, owning the relationship with your customer, linear commerce, DTC brands, and how Web has built 2PM.

Listen to this episode from Village Global’s Venture Stories on Spotify. Rex Woodbury (@rex_woodbury) of Index Ventures joins Erik on this episode to discuss:- Where he’s looking to invest in the creator economy.- Why authenticity and vulnerability are replacing performative and status-driven social media.

Visuals

FT

Axios

Tweets

I hope nobody gives gyaan on this - "if it was Bitcoin, it would have worked".

Not even close.

Transaction scaling is a fucking hard problem. And very very very few orgs have really solved it at global scale.

Like VISA

https://t.co/rF8BG8Uagj

Thread: I have great respect for @dandolfa. But I think that here he, like many other proponents of CBDC, too readily assumes that it can be viewed as a "public option," that is, something costless to a public that doesn't have to use it if it doesn't wish to. https://t.co/KQMVNaD4C5

Ben is of course right - #WallStreetConsensus is a development paradigm invented for the Global South, but could easily travel up North to satisfy the portfolio glut's hunger for infrastructure assets. https://t.co/Hm6qWM6UfS

If you don't want these updates anymore, please unsubscribe here.

If you were forwarded this newsletter and you like it, you can subscribe here.

Created with Revue by Twitter