Honest in the streets, crooked in the sheets

Honest in the streets, crooked in the sheets

Hi, you are fortunate enough to be reading yet another edition of The Tipsheet—the Financial Times for aspiring income redistributors (scamsters). You are welcome.

Ok, this email might break in your inbox because you’re too poor to afford a good phone. So to help all you poor people, here’s the link to the full post so that you can read this on your browser or save it to your Pocket or Instapaper.

Guaranteed income scheme

There are two ways to earn money. You can wake up every day, go to the office you don’t want to, work with people you don’t like and do things you hate. You have to say “synergy”, “think outside the box”, and “circle back” 36 times a day and be miserable. Then there are jobs where your effort is inversely proportional to the money you make—lesser the work, more the money.

You might be thinking that such a job cannot possibly exist.

You’re wrong. That’s why you’re poor!

It exists, and it’s called asset management!

Set aside the passive fund managers. I’m talking about active fund managers.

The job of an active fund manager is to beat the benchmark and make you galeej (filthy) rich, but most people suck at it. I mean, they really suck, like Ram Gopal Varma Ki Aag level suck, but it doesn’t matter.

The way I see it, there are five types of asset managers.

1. Honest to a fault

There are the naive, idealistic fund managers. They actually work hard and honestly try to deliver performance instead of taking the easy way out of hugging a benchmark and getting fat by charging ~1% of the AUM for doing nothing.

I’ve never liked these honest people. They are a kalank on this planet. You shouldn’t aspire to be like these honest people in life. They are setting the wrong examples.

2. Curtain Ke Peeche Kya Hai

Then there are the asset gatherers. All they care about is getting rich from overcharging and underdelivering. These are the real role models.

They are honest in the streets, crooked in the sheets.

But, here’s where the geniusness of these people comes. They know that most investors are dumb, stupid and lazy. They know that investors are illiterate and don’t understand things like measuring performance and calculating fees. So, they figured, why even bother with ridiculously silly things like delivering performance and justifying their fees. They’re not stupid! They just hug the benchmarks and rarely bother to do anything original. They honestly work hard to not work hard.

Instead of doing useless things like delivering performance, they focus on productive things like asset-gathering because more AUM = more chance to redistribute money from low-IQ investors.

This is a guaranteed income scheme. It’s like a government bond—you keep getting money no matter what.

Active in the streets, passive in the sheets.

But, just in case there are savvy investors who understand that they’re not getting their money’s worth, they’ve figured out a solution—talking out of the wrong part of their lower abdomen.

To confuse the smart people, they say meaningless stuff like this👇

What they say: It’s a stock pickers market. What they mean: We really suck at our jobs.

What they say: Buy & die. What they mean: We will continue not to do our job, so please don’t sell, hold for 100 years. We need time to redistribute your money.

What they say: It’s a cyclical bear market in a structural bull market. What they mean: We are overweight on ITC, and it’s underperforming a liquid fund.

What they say: Invest in the India growth story. What they mean: We know you’re going to sell, so we are trying to use patriotism to guilt-trip you into not selling so that we can continue to charge you for not doing our job. Thanks.

What they say: We’re cautiously optimistic. What they mean: Hi, good morning. We have no clue what we are saying. This is like homework, we have to make something up.

What they say: The Fed has distorted the market. What they mean: We chanted Warren Buffett 21 times and picked some stocks, but 12-year-old kids trading penny stocks are outperforming us 😭😭

What they say: There’s lots of cash on the sidelines. What they mean: Please, please, don’t sell. I won’t make my bonus for doing nothing.

And my personal favourite: We’re in a new normal.

Reread these things, and I’m sure you will appreciate the brilliance of using a lot of words to say absolutely nothing. And given that a lot of investors tend to be total idiots, they fall for this fancy-sounding nonsense, and these people continue charging money for doing nothing. Brilliant, ain’t it?

Having said that, this fixed-income strategy of income redistribution (scamming) has some risks.

In 2019, The Financial Conduct Authority (UK SEBI) found that a lot of so-called active managers in the UK were passive—malnourished sheep in hungry wolves clothing. Here’s what the FCA had found in 2016:

We have concerns about how asset managers communicate their objectives to clients, in particular how useful they are for retail investors. We find that many active funds offer similar exposure to passive funds, but some charge significantly more for this. We estimate that there is around £109bn in ‘active’ funds that closely mirror the market which are significantly more expensive than passive funds.

It reviewed 96 active funds, of which only 25 were true to their label—active in the streets and benchmark agnostic in the sheets. The rest were just scamming by hugging the benchmarks. The FCA forced them to pay back £34m and fined Janus Henderson £1.9m for misleading investors.

Not just UK, Ireland also found that they had a closet indexing problem and launched investigations and imposed fines. Last year, the Norway Supreme court fined DNB asset management for closet indexing.

The European Securities and Markets Authority (ESMA), a while back, had found that well over a trillion euros are stuck in closet index funds. That’s a bloody trillion with a capital T! The problem has only gotten worse since then.

Based on Morningstar data we estimate the European funds industry to be approximately €8tr in 2016, implying on our estimates that €1.2tr could be defined (at its loosest definition) as closet indexing, with €400bn (at its tightest definition) coming under particular scrutiny.

In the Indian large cap funds space, 1 in 3 funds are closet index funds:

While average R2, a traditional measure of active management or selectivity, between returns of large-cap schemes in our sample and those of a large-cap index tracking fund, has remained stable at 0.93 through the period, there have been key changes to selectivity of schemes. 1 in 3 funds every month have had R2 >= 0.95, a popular benchmark for “closet index” funds. We show that the pandemic has significantly impaired the returns from selectivity as seen in the jump in the average R2 from 2020 and is a significant driver for the drop in 3-year alpha between 2018-2021.

But compared to fees they redistribute from individual investors, these fines are a drop in the bucket. They can continue doing the same old thing. For now, this fixed-income strategy of income redistribution (scamming) works. Risky, but it works.

3. Asset management Greta’s—Sustainable in the streets, dirty in the sheets

Let’s say you are a fund manager working hard day and night not to work hard—you just hug the benchmark, Netflix and sleep. Let’s say, suddenly, some of the smart investors in your utterly useless fund start withdrawing money. Well, it’s a problem.

But lucky for you, our planet is burning. We’re all probably gonna die, but it’s bloody good for your business. Global warming is the best thing to have happened to asset managers since the invention of the percentage of the AUM fee model.

So, until 3 years ago, all you were doing is to publish 20 PDFs a day with random charts and conduct 10 “it’s a new normal” webinars to distract the simpleton clients and take their money. But now that they are withdrawing their money, you need to change the script.

To stop people from pulling money out, just rename all your useless closet index funds as “green”, “social”, “sustainable”, and “ESG.” Oh, and you can’t just rename, you have essentially become the asset management Greta and start occasionally saying, “how dare you.” That’s it. It’s that simple.

You might think this doesn’t work.

You’d be wrong.

There are plenty of idiots around the world who believe that they can stop global warming and save the planet by investing in green and ESG funds. If there are idiots, not taking advantage of their idiocy is a sin. Even Jesus said so:

Thou shalt take advantage of idiots and part them from their money. Exodus 12:11

If your fund is useless, that’s not an issue—just add “ESG” to the name.

Markku Kaustia and Markku Kaustia analyzed existing funds that rebranded themselves as “green” and “sustainable”, and they found that investors do fall for these green and sustainable crap. What’s more, the funds which had the lowest flows on average were more likely to rebrand themselves. 👏👏👏👏👏

We first document that a self-designated ESG label helps mutual funds attract more flows than their non-ESG peers with otherwise similar characteristics. We show this happens even if labeling the fund as ESG is in conflict with Morningstar’s objective Globe ratings. This is consistent with greenwashing motivations.

Funds attracting below average flows are more likely to be repurposed as ESG funds. On average, a 10 percentage point decrease in the percentile rank of past 3-year flows increases the probability of a fund being repurposed by 0.02 percentage points. We find no evidence that ESG-repurposing behavior improves flows or performance, at least in a short-term window after the repurposing event

You can continue to be a hypocrite after you rebrand your useless closet index funds as “ESG.” You can even go full Greta like Larry Fink and write letter after letter asking everyone to change things, go green, and berate people for not thinking sustainably.

But you can do the exact opposite in practice because people are idiots, and nobody cares about saving this planet. Fund investors don’t care if you support companies that destroy the environment, exploit workers, and have terrible gender equity.

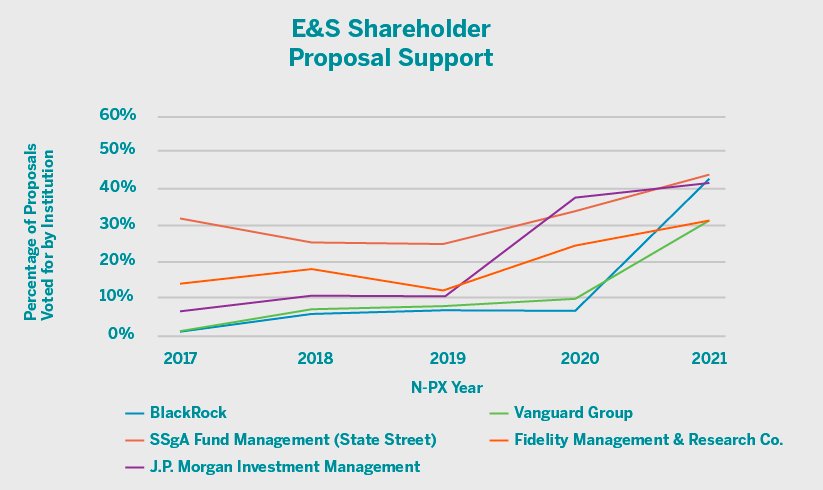

Here’s how Vanguard & BlackRock—the two largest asset managers vote:

Surprisingly, Rao found that the Vanguard Social Index Fund voted against almost all environmental and social resolutions over the time examined. The fund also voted against shareholder resolutions requesting disclosure of board diversity in every single instance since 2006.

In addition, both Vanguard and BlackRock in 2019 voted against proposals requesting disclosure of board diversity and qualifications at Apple, Discovery, Twitter, Facebook, and Salesforce.“What we found was really not good,” Rao said. “I would give Vanguard a D. Their social index fund is one of the largest ESG funds in the market, particularly in the retirement space. It’s the oldest fund, and it votes most of the time against disclosure on environmental and social issues.”

Here’s an even brutal analysis by ShareAction:

BlackRock, for one, opposed 47% of climate resolutions, State Street 58%, and Vanguard 62%. The “Big Three” also voted against a majority of resolutions related to social and governance issues, such as closing executive and gender pay gaps.

Assuming that people still harass you to support ESG issues, you can throw them a bone and support some while opposing most ESG shareholder proposals. This is precisely what the largest US asset managers are doing. Up until last year, they voted against pretty much all ESG issues. But in this years’ proxy voting season, they supported about 30-40% of the proposals. This is enough to shut those annoying green idiots for a while.

4. The content marketers

Then there are hedge funds. They are basically costly mutual funds for galeej (filthy) rich people. Most rich people are either too stupid, or they don’t care. Hedge funds did a pretty smart thing staying exclusive. The smarter hedge funds even stop accepting new money occasionally.

They’ve figured out human psychology brilliantly—we want what we can’t have.

Given that hedge funds are exclusively meant for only some people, they’ve become a status symbol of sorts. Rich people knock on their doors to willingly lose money.

Hedge fund managers are often called the “masters of the universe”; they’ve built this mystical aura around themselves. People think that hedge funds are all-seeing, all-knowing and are always making money and don’t know the meaning of the word “loss.”

Well, it’s not true, but hey, like Albert Einstein said:

Other people’s stupidity is your margin

To be fair, hedge funds were indeed the masters of the universe once upon a time but not anymore. Hedge fund performance pre-2008 made the returns of the S&P 500 look like a liquid fund. But post-2008, the hedge fund managers went from being masters to that guy travelling on a train to Panvel.

But it doesn’t matter. Look, humans are lazy by default. They hate doing things, and they hate change. In fancy speak, this is called “inertia”, and as a hedge fund manager, this is a gift for you. No matter how horrible your performance is, most people won’t care because taking out money requires effort, and investors are lazy!

Larry Swedroe, one of the most prolific finance curators and writers of our time, recently summarized the latest research on hedge fund performance. Here are a few excerpts:

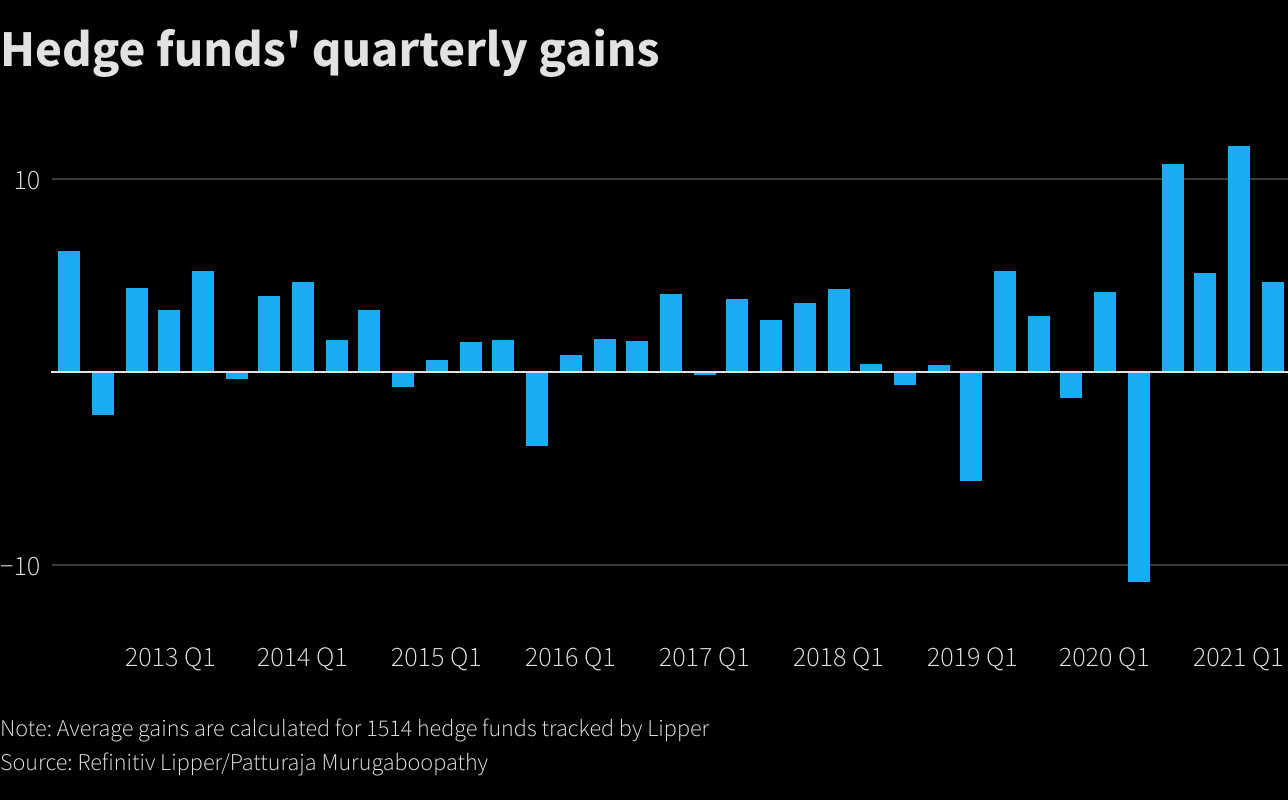

From 1998 through 2002, the hedge funds produced an incredible alpha of 9.0 percent. That performance fuelled the growth of the hedge fund industry. However, from 2003 through 2007, their alphas disappeared, falling to -0.7 percent. And from 2008 through 2012, the alpha became -4.5 percent.

Sullivan asset-weighted the returns and found that due to the increase over the full period, hedge funds had destroyed almost $46 billion on a risk-adjusted basis. And alpha has been persistently negative since 2008.an equally weighted hedge fund index provided a cumulative return of 225 percent from 1997 through 2007, far outpacing an equally weighted stock and bond portfolio, which generated a cumulative return of 125 percent. Those returns led to the dramatic increase in cash flows, as investors wanted a “piece of the pie.” However, from 2008 through 2016, the hedge fund portfolio earned just 25 percent compared to the 70 percent return of the stock and bond portfolio—the underperformance occurred when the industry had much greater assets under management.

The best part is that hedge funds have a brilliant fee structure. They charge a fixed fee of 1-2% and take 10-20% of the profits they generate above a certain level—commonly known as the 2 & 20. So no matter what happens, they make money. Talk about a guaranteed income scheme.

It didn't matter for a long time since they were actually delivering performance. But since 2008, they have become pretty much a costly mutual fund. Some smart people figured this, and hence there’s been fee compression across the board:

But here’s the bestest part, it wasn’t 20 & 20, it was more like 2 & 50:

We study the long-run outcomes associated with hedge funds’ compensation structure. Over a 22-year period, the aggregate effective incentive fee rate is 2.5 times the average contractual rate (i.e., around 50% instead of 20%). Overall, investors collected 36 cents for every dollar earned on their invested capital (over a risk-free hurdle rate and before adjusting for any risk).

As Aristotle famous said:

Fund managers get alpha, you get ghanta🔔

Ok, so let’s say you’re a hedge fund manager. You were a star one upon a time, and your surname was “Alpha”, but now, you've become “kya beta?”, what do you do?

You just become a content marketer.

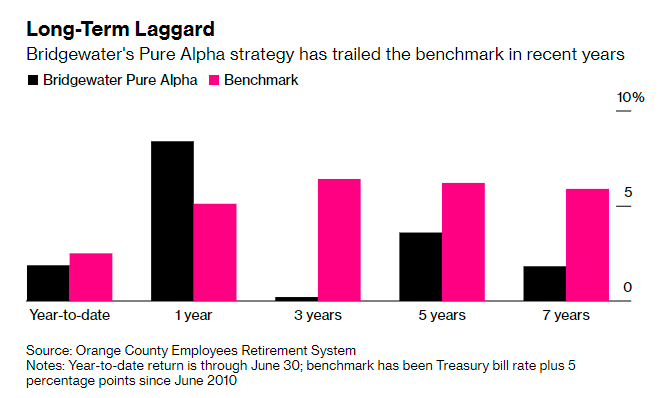

There’s a long-running joke that Ray Dalio, the founder of Bridgewater with over $160 billion in assets, is one of the best content marketers ever. I mean, not to pick on him or anything, but the number of media appearances and blog posts is inversely correlated to Bridgewater’s performance:

It’s not just Bridgewater. Any fund that’s loud, 9 out of 10 times it’s because their performance sucks and they are bleeding assets.

There’s an old saying:

A hedge fund is compensation scheme masquerading as an asset class

Given the horrible performance of hedge funds, predictably, several customers are fleeing them. Here’s the sad story of the Joaquin County pension fund:

San Joaquin’s consultant, Pension Consulting Alliance, first recommended putting Bridgewater under review in November 2017. At the time, the Pure Alpha II macro fund had posted annualized returns before fees of just 6.9 percent for the five years ended Sept. 30, 2017, according to a report on the pension fund’s website. After paying a fixed fee of 3.69 percent, the pension fund ended up with a 3.1 percent annualized return, meaning that Bridgewater took more than half of the money it made for the county fund in those years.

Even the Orange County pension got rid of Bridgewater. You know things are bad when your hedge fund becomes accessible to retail investors who don’t want it.

But for every smart pension fund that flees hedge funds, there will be 20 dumb investors that invest in them:

I mean, if you are a hedge fund manager and your fund is bleeding assets, there are worse strategies than always going on CNBC and calling “cash is trash.” You gotta do whatever you need to keep then 2 & 20% shekels coming.

Investor: Hi

Hedge fund manager: Hello, how can we steal money from you today? Sorry, help you today?

Investor: Why are you guys underperforming?

Hedge fund manager: These are challenging times, but we are cautiously optimistic.

Investor: But what happened? Why are you underperforming a govt bond? Why are you still charging 2 & 20?

Hedge fund manager: Our performance was severely impacted because other people were selling the stocks that we bought.

Investor: Huh, what?

Hedge fund manager: We are in an unprecedented environment where 18-year-old kids and The Fed are causing a bubble that is causing all stonks to go up?

Investor: So you are underperforming teenagers?

Hedge fund manager: We just want to protect you. These are challenging times, and this is a 14 standard deviation event that has increased volatility and correlation in a highly leveraged risk-on market that’s disconnected from fundamentals due to The Fed and teenagers. Our goal is to protect the downside while sacrificing upside to hedge against black swans and grey donkeys.

Investor: I’m sorry for calling you. Forgive me!

As long as you sound fancy and confuse the hell out of people, there will always be people willing to donate money for your welfare voluntarily.

People don’t buy numbers, they buy stories. As long as you can tell good stories which are divorced from reality, you will always have people willing to part with their money.

Asset management is 10% fund management, 90% storytelling! Otherwise, how can 70-80% of the managers who don’t even touch the benchmark, let alone beat it, stay in business?

It’s the greatest income redistribution opportunity of all time. A true fixed income strategy of income redistribution.

5. Just steal it

Not everybody is patient in life. It’s very important to lead your life according to your psychological makeup. So, if you’re impatient and don’t want to make money slowly and gradually from dumb investors by delivering horrendous performance, you can indeed steal money in one go.

Take the case of China Fortune Land, a leading developer of industrial parks in China. It’s also backed by Ping An, the largest insurance company in China. China Fortune became the victim of China’s “The three red lines”—rules to curb excessive leverage in the real estate sector.

First, it couldn’t refinance and defaulted on about $1.2 billion in debt. Then just yesterday, it disclosed that it lost contact with China Create Capital Ltd. It had invested $313 million in China Create Capital and was promised 7% to 10%. Now, apparently, China Fortune is unable to locate China Create Capital. Not reachable. Bad network!

So the lesson here is, set up an asset management company in a tax haven like the British Virgin Islands—which is where China Create Capital was registered—and promise high returns. Inevitably someone stupid like China Fortune will fall for it, and after some time, once you have collected enough money, just take that and run away.

Once you run away, you can invest that stolen money in crypto and make that money earn more money. Once you have made more money on crypto, you can invest that money back in Chinese govt bonds to earn a predictable rate of income. This is called prudent financial planning.

Goody-good reads

Markets

“To The Moon is not fundamental analysis. It is an inducement. It is an encouragement of belief. And the only thing that is fueling that rocket ship To The Moon is the credulity of others,”

ESG nonsense!

VCs are saving the world

Techmology

Behave

Crypt…oh!

We’re all going to die!

Perhaps as practice, to gird ourselves for the worst-case scenario. What if it never ends?

Could tinkering with photosynthesis prevent a global food crisis?

Non-finance fascinating thingies

This is the last issue for this year, and with that, It’s a wrap on this absolutely horrible year. Every single day of this year was a lower circuit for a lot of us. I’ve no idea what the next year has in store for us. But if we have an even more horrible year than this one, then that dude/dudess in the sky must have a really sick sense of humour.

But I hope all of you have a wonderful and scammy year ahead, except for all the fund managers hugging the benchmarks and scamming idiots. I hope it’s filled with a lot of income redistribution opportunities.