Efficient market hypothesis my a**

The Tipsheet

Hello peoples. Things are becoming bleak with this damn virus, so please stay at home, if you’re privileged enough, many of us aren’t. Please take all the necessary precautions, stay safe and try not to die by doing dumb things.

The stock market, hands down, has to be among the most entertaining places on the planet. It provides so much entertainment for us all. This week’s Tipsheet is full of these entertaining incidents. Since I’ve started writing this, I’ve been partly clueless if you guys like reading this thing or it’s utter dog shit. So, I’ve added a feedback form at the end of the post. If you don’t give your feedback, you’ll underperform Suzlon for the rest of your life.

Here’s this week’s Tipsheet.

Top of the news

What’s in a name?

So, typically when there are big events, and you want to trade them, you look for trades where you have the best chance of making money

. For example, if many people are dying, buying FMCG companies is a bad idea. Because research shows that dead people consume less. On the other hand, if there are listed companies like mortuaries, body bag manufacturers or medical oxygen companies, you can make a lot of money.

Generally, you search for stock with those keywords and look for stocks like Sunshine Body Bag Manufacturing or Bombay Oxygen Corporation. This is what’s been happening over the last couple of weeks. With the spike in COVID-19 cases and deaths, there was a Medical Oxygen supply shortage across India. So investors started searching for stocks with the name “Oxygen” because they were betting that these stock would go up because of the high demand.

And Bombay Oxygen Corporation figured at the top of the results. People started buying the stock and the price skyrocketed.

But there was a tiny problem. The company no longer manufactures Oxygen but is rather an NBFC

The Company’s primary business was manufacturing and supplying of Industrial Gases which has been discontinued from 1st August, 2019. The Company has been issued a Certificate of Registration from the Reserve Bank of India, Mumbai dated 31st December, 2019 for carrying on the business of Non-Banking Financial Institution (NBFC) without accepting Public Deposits.

And predictably, people started shitting on The efficient market hypothesis (EMH) and its creator Eugene Fama. One angry reader sent me this image and said, “EMH is as f****** useful as a f****** erotic novel like this f****** one. How can a f****** theory f****** disproven by a bunch of f****** idiots win a f****** Nobel prize?”

This isn’t the first time this is happening.

Changing stock names and investors confusing stock tickers have been causing sharp spikes in stock prices for a long time. Here’s an old study documenting the impact of name changes on stock prices at the height of the tech bubble:

We document a striking positive stock price reaction to the announcement of corporate name changes to Internet related dotcom names. This “dotcom” effect produces cumulative abnormal returns on the order of 74% for the ten days surrounding the announcement day.

We conduct a search for pairs of companies with similar names/ticker symbols. Between 12% and 25% of such pairs exhibit co-movements in trading turnover, which we attribute to investor confusion.

My personal favourite name change pump and dump was the one involving The Long Island Ice Tea Corp back in 2017. This was the previous crypto peak, and there was the same mania we see today. There was an insane demand for easy crypto exposure, given that it was still relatively difficult to buy and sell Bitcoin back then. So a bunch of companies started making vague statements that they would “use blockchain”, and their prices would skyrocket. But Long Island Ice Tea, a juice maker, decided to take it one step further. It changed its name to Long Blockchain Corp, and the stock at one point was up more than 450%

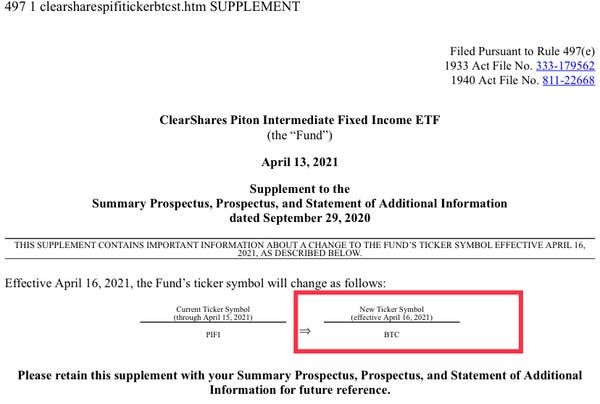

This intermediate-term bond ETF has apparently decided ‘BTC’ would be a better ticker than its current ‘PIFI’. Wonder why. 🤔 https://t.co/qUx4eoz5sb https://t.co/rsbTNm4asQ

Short end

There’s been a long-held theory that stock markets are a place for companies to raise money and that they also help in the price discovery of securities, aka Ben Graham’s weighing machine. The way price discovery works is that the prices of good companies go up, and those of bad companies fall or go to 0. It seemed like this theory was true until last year when a bunch of bored teenagers came together, stole money from their moms and started a revolution on Wall Street. The revolution was called pump and dump.

These teens with bad breath, attention deficit and adrenaline imbalances started pumping stocks regardless of whether they were “good” or “bad”. Now, for effective price discovery, you need two people – grownups bullish on a stock and bearish. If everybody is bullish, shit won’t work as we saw in the case of Pakistan, when it banned selling. This is where short sellers come in. These people make money by betting that the prices of “bad” stocks will fall. But since they bet against companies, they are among the most hated people in the markets, so much so that short sellers get constant death threats, have to deal with lawsuits, harassment and other forms of non-medieval torture.

I remember Marc Cohodes, a legendary short seller saying that there has to be something mentally wrong with a person if he chooses to be a short seller. Short selling is among the toughest ways to make money in the stock market. The problem is, most of the shorts tend to be dubious, scammy companies and these stocks, as we saw this year in the US, can move 100-300% in a day before falling. And if that happens, you’re buggered, as we saw in the case of stocks like Gamstop, because you need to post additional margin. But short sellers are incredibly important for the markets. They give regular enemas to the stock market by finding and shorting fraud and dubious companies.

And this topic is super important given that we are in one of the longest bull markets in history. And bull markets are the best times to be a fraudster. A Minsky moment, if you will:

The more general concept of a “Minsky cycle” consists of a repetitive chain of Minsky moments: a period of stability encourages risk taking, which leads to a period of instability when risks are realized as losses, which quickly exhausts participants into risk-averse trading (de-leveraging), restoring stability and setting up the next cycle. In this more general view, the Minsky cycle may apply to a wide range of human activities, beyond investment economics.

Here’s a nice profile of Carson Block of Muddy Waters Capital, who’s made it his life’s mission to call out frauds. He’s perhaps most well known for calling out the fraud at Nikola and reverse listed Chinese companies.

Not all of Block’s short campaigns have worked out, of course. Yet over the past five years, Muddy Waters has produced an annualized return of roughly 19 percent — and that’s after a 2.5 percent management fee and a 30 percent performance fee.

He’s become so influential at a mere mention of a company without content is enough to send stock tumbling:

Muddy Waters’ research may be highly lauded, but most people don’t wait to read it before making the trade. Stocks fall immediately after Block names them — and sometimes before: High-frequency, or algorithmic, traders constantly scrape his website looking for a new short report, sometimes even seeing the name on the URL before it becomes public, according to Block. In Europe, where regulations force him to disclose short positions, the mere notice that he was short one stock — Solutions 30 — led it to tumble 20 percent in a day.

And if you are wondering why you don’t hear of such people in India, short selling is tough in India due to a whole host of reasons.

A nice piece on the short selling tactics of some of the best in the business like Jim Chanos.

Some history of short selling.

Some ramblings on how shorts can be manipulated

Arche…goes on and on and on!

The Archegos saga has been super entertaining. I think it’s partly because big banks are hated by pretty much everyone, and watching one lose money is a bit gratifying. Like I had mentioned last time, we maybe never truly know what went down. We have to draw conclusions based on the steady stream of stories that are trickling out.

At its core, as Marc Rubinstein writes in the Net Interest, investment banks make money by buying, selling and matching risk:

In short, investment banks traffic in risk. Buying and selling risk can be a profitable business, although it’s not as profitable as it used to be. Coalition Greenwich is an analytics company that tracks global investment bank revenues. The people there reckon that last year, investment banks earned nearly $200 billion of revenue, the most in over a decade. Sales and trading made up almost $150 billion of that, the rest being advisory and underwriting fees. Prior to 2020, operating margins in the industry had been coming down, but last year they jumped to 44%. Such high margins require a lot of capital to generate.

Meaning, if you are an investment banker, you need to know how much risk you have on your hands. If not, it’s a bit like trying to do surgery by watching YouTube videos. You can do it, but no guarantee you’ll have your left kidney intact. This seems to have been the case with Credit Suisse, which had nearly $20 billion exposure to Arche…going on Capital as well.

The U.S. family investment firm’s bets on a collection of stocks swelled in the lead-up to its March collapse, but parts of the investment bank hadn’t fully implemented systems to keep pace with Archegos’s fast growth, the people said.

Credit Suisse Chief Executive Thomas Gottstein, and Chief Risk Officer Lara Warner, who recently departed the bank, only became aware of the bank’s exposure to Archegos in the days leading up to the forced liquidation of the fund, people familiar with the bank said. Neither Gottstein nor Warner had been aware of the fund as a major client before that, these people said.

This shit is too funny 😂🤣🤣

5 reads

Trying something new after readers sent some feedback. Instead of sending multiple links, which will rot in your bookmarks, I’ll send the best 5 links. Let me know if this is good or if I should stick to the previous format of curating all the links.

Did you enjoy reading this thing? Why don’t you annoy your friends and followers by sharing on social media things?

If you don't want these updates anymore, please unsubscribe here.

If you were forwarded this newsletter and you like it, you can subscribe here.

Created with Revue by Twitter