It's only a scam if you get caught

It's only a scam if you get caught

The antitrust and market concentration edition

Hi there, you unsmart person, you are welcome. I’m the king of the best post openings! With this version of Tipsheet, I just increased your IQ by 7.8 points. You’re welcome. I was on a break because I was waging biological warfare with a virus. It was like a really shitty Micheal Bay movie also called a Micheal bay movie.

This post is a bit long because I’ve to make you smart, don’t you dare complain. The post might break in your email. Here’s the link to the post if you want to read it in your browser or Pocket or Instapaper.

Like I said in the last issue, something is only a scam if you as an individual do it. But if companies do scammy things, it’s not an issue because they have figured out how to scam successfully and get away with it. If you scam and get caught, you go to jail. If companies scam, they call it margin expansion.

What scam am I talking about today, you ask?

I’m talking yugee companies, monopolies, oligopolies, market concentration, and increasing market power—all terms used to describe how markets are getting concentrated around the world. In the past 40-50 years, markets across the world have increasingly become concentrated. Just three to four companies in each sector have cornered vast swathes of the markets, and they’ve become like the mafia.

Rising market concentration is due to an all-you-can-eat buffet of reasons like poor antitrust laws, regulatory arbitrages, regulatory capture, predatory pricing, mergers & acquisitions, stunningly stupid economic beliefs, and rising barriers to entry, among other reasons.

The result is a highly unequal world. A few large firms have become increasingly large, while the smaller companies have become economically malnourished.

The fat poster children of this trend have the big tech companies like Facebook, Google, Apple, Amazon, and Microsoft. But tech isn’t the only sector where concentration has been rising; all sectors across much of the words have become increasingly concentrated over the last 30-50 years. Large corporations have taken income redistribution global. They’ve achieved economies of scale at running these income redistribution schemes (scams).

Some companies have become big and redistributing income (scamming), ok, big deal. Why should you be bothered, you ask? Ok, the first thing is, I’m not going to call you stupid for asking such a question. I’m not saying you aren’t stupid, but I am not saying you are either.

As big companies get bigger, market power becomes concentrated among them. When a small set of companies have what I like to call “I have a big brinjal🍆” syndrome, it leads to all sorts of saas-bahu level problems. Starting with labor share, reduced ability of workers to bargain (stagnant wages), a decline in R&D, reduced innovation, reduced dynamism, reduced competition, regulatory capture, increasing accrual of profits to companies, income inequality, problems starting flowing out like a certain part of body behaves during a bad diarrheal episode🌊.

Has market concentration (scamming) increased?

Let me start by saying economists are like dogs and cats—they goddamn never agree on anything. Their entire lives are searching for moments where they can say “but”. That’s what happiness means for them—saying “but”, not even butt, but rather just “but”. It’s the same problem with market concentration. Measuring market concentration is hard, and attributing causality is even hard.

On the other hand, the thing you need to know about economic research is that it can directly affect policy outcomes. There’s a lot on the line for certain companies and interest groups if regulations they don’t like are passed. So, big companies and big income redistributors have an incentive to muddy the waters or do highly extra-legal shit. Think tanks, special interest groups, and industry trade groups and associations funded by the big companies regularly publish bullshit, I mean dubious research to cast doubt on legitimate research:

These lobbying—sorry, research—centers don’t publish anything in any academically meaningful sense, and never will, but they produce glossy pamphlets with very polished words (they know how to write) and, often, with serious misinterpretations of economics. In fact, very few of these pamphlets are written by economists with credentials. Basically, these centers use envoys under semi-academic camouflage. Their funding is opaque. Two names that come to mind in the context of antitrust and competition policy are the Global Antitrust Institute (GAI) at George Mason University, and the International Center for Law & Economics in Portland, Oregon.

There was a high-profile incident back in 2017. Open markets Institute, which was part of the New America think tank, was kicked out of the group. The reason was—Barry Lynn, the institute’s head, congratulated the European Union for imposing a fine against Google. Eric S Schmidt, the then chairman of Google, was a donor to New America. Oh, and George Soros also funds open Markets. When poor people disagree, they fight with their fists. Rich people fund think tanks. Their pissing contests are on a whole new level🤦♀️

So, yeah, back to the point. There’s a lot of research that shows market concentration has increased around the world. Pretty much all economists and scholars on the left, right, south-west and 73% centre right agree on the point. The disagreement is when you start looking at things at a micro-level.

Research in the last couple of years has shown that while concentration at a national [1, 2] and global level has increased, it has reduced at a local level [1, 2]. To be fair, this is also party due to issues with data and how industries are classified. Depending on which data set and classification you use, you can end up with markedly different conclusions.

What causes increased market concentration?

This is where things get a little messy. There are two schools of thought. On the one hand, some people believe that companies become bigger and generate profits because they have the best products and services. On the other hand, you have people who think that market concentration and the rise of monopolies are a result of the failure of antitrust regulations and regulatory and political capture by these companies—in other words, they run income redistribution schemes (Scams). So which hand is right? This reminds me of a famous quote attributed to George Bernard Shaw:

If all the economists were laid end to end, they would not reach a conclusion.

It’s the same with this debate. Moreover, economics has an unnatural fetish for accuracy. Given just how infinitely messy and complex markets and economies are, this debate will be just like the other great debate of our times: Is Shashank Redemption the greatest film of all time or Ram Gopal Varma Ki Aag?

How bad are things?

Let’s survey the shitshow, shall we?

Top 4 AMCs in India control over 50% of all the assets.

BlackRock, State Street, and Vanguard are over 80% of the ETF market. These three firms combined are the largest shareholders in over 40% of all listed US companies.

Just 3 telecom companies—Reliance Jio, Airtel, and Vodafone Idea—which is a dead company walking— account for 90% of the market.

National Stock Exchange of India (NSE) is a near-monopoly with 93% of cash market volumes, 100% of equity derivatives and 60% of currency volumes. BSE, its next competitor, doesn’t even register on the scale.

Nestle has an 85% market share of the Indian baby food market.

Bayer (Monsanto), BASF, Chem China (Syngenta), Corteva, Dow-Dupont and Limagrain account for more than 60% of the global seed market and 75% of the agrochemical market.

Anheuser-Busch, SAB Miller, and Heineken accounted for over 70% of the global beer market profit pool. Anheuser-Busch alone holds a 30% global beer market share.

YKK is the world’s largest zipper manufacturer, with a 40-50% market share.

Penguin Random House, Simon & Schuster, Hachette Book Group, and Macmillan pretty much are the entire book publishing industry.

Elsevier (SSRN), Taylor & Francis (Tandfonline), Wiley-Blackwell, Springer and Sage are over 50% of the academic journals market.

Illumina has over 80-90% of the gene sequencing market.

EssilorLuxottica owns over 40+ eyewear brands like Ray-Ban, Oakley, Crizal, Varilux and licensed fashion brands like Chanel, Armani, Prada, Ralph Lauren, Dolce & Gabbana and Ralph Lauren, among others.

Walgreens, CVS, and Rite Aid are 67% of the US drug stores market.

REV Group and Braun Industries are 83% of the ambulance manufacturing market.

Johnson & Johnson, Novartis, The Cooper Companies, and Bausch Health control 77% of the contact lens market.

Boston Scientific, Abbott Laboratories, and Medtronic control 89% of the pacemaker market.

Hillenbrand and Matthews control 82% of the Coffin and Casket manufacturing market.

Mindgeek controls 70% of all adult websites.

Nestlé, J.M. Smucker, Supermarket Brand, and Mars control 97% of the cat food market.

Barilla, Ebro, and Treehouse control 78% of the pasta market.

Grupo Bimbo, Flowers Food, Campbell Soup and Lewis Bakery control 60% of the bread market.

General Mills, Kellogg, and Post Holdings control 72% of the breakfast cereal market.

Coca-cola, Pepsi, and Keurig Dr Pepper control 93% of the carbonated soft drinks market.

Danone and Steamicks control 82% of the Soy milk market.

Blue Diamond, Danone, Califa Farms, and Coca-cola control 81% of the refrigerated almond milk market.

Conagra, General Mills, Vigo Importing, and Brooklyn Bottling control 98% of dry dinner mixes with the meat market.

Conagra controls 91% of the single-serve prepared sloppy sauce market.

Pepsi controls 87% of the dip market.

Conagra, Campbell Soup and Weaver popcorn control 86% of the Popcorn market.

Hershey, Mars and Lindt are 80% of the chocolate market.

MOM Group and Hain Celestial control 94% of the single-serve yoghurt/yoghurt drinks market.

Dongwon, FCF Fishery, and Thai Union control 84% of the tuna market.

Google has a 90% market share among search engines.

Google Android has a 70% mobile operating system market share and Apple iOS about 20%.

Amazon has a 50% market share of retail e-commerce in the US and 30% in India.

Microsoft Windows has an 80% market share.

This data is thanks to the phenomenal work of Open Markets Institute and The Guardian.

These are just a few examples. The concentration problem runs far and wide. The top 4 companies 70-80% of major products, services, and markets around the world. It’s easy to jump to the conclusion that concentration of market power is always bad, but it needn’t be. But unfortunately for us, a disproportionate number of companies that grow to be large start to do shady and illegal shit. These scams can harm consumers quite a bit.

Shit like:

There’s no better example of just how evil companies can get than Dow Chemical. It has settled countless cases of poisoning people. It’s among the largest mass-murdering companies. If you kill someone, it’s murder. If chemical companies poison and kill people, it’s a court settlement. It paid $670 million to settle a water contamination case as recently as 2017. It was knowingly leaking chemicals and making people sick. There have been countless cases like these. Remember the movie, Erin Brockovich?

R. J. Reynolds, the tobacco giant, wanted to turn kids into smokers and had designed cartoon ads to seduce them.

Exxon knew about climate change as far back as 1977 but spent millions for decades funding climate change denial research and hiding its own.

Monsanto has sued countless farmers for replanting seeds from a harvest. They’ve stopped farmers from reusing seeds because the seeds are apparently their intellectual property. They’ve won millions in settlements from such cases. They’ve even sued farmers when seeds blew over from neighbouring farms after a harvest and germinated.

People have repeated accused Walgreens and CVS of price gouging, even for regular generic drugs. In some cases, they’ve sold drugs at prices between 7X 1000% more.

At $ 10,949, the US has the highest per capita health spending in the world. Their healthcare sucks, to put it succinctly. Decades of hospital mergers have made the healthcare system incredibly concentrated and costly. This has led to prices increasing by as much as 40%.

The Boeing 737 Max crash, which killed 346 passengers, was a classic case of regulatory capture. In order to compete with Airbus, Boeing cut corners with aircraft development. The Federal Aviation Administration (FAA) knew what was happening and was whistling show tunes.

A recent lawsuit alleged that Google and Facebook colluded to divide the advertising market between themselves. I mean, being a duopoly is boring. Normal people watch TV when bored. Big companies collude and form cartels when bored.

People like Martin Schmalz and Marshall Steinbaum have raised concerns that common ownership of stocks by the same asset managers can lead to anticompetitive practices like collusion.

Just this week, Reuters broke a story that Amazon in India was creating copycats of products being sold on its platform. Now, that in itself is not bad. But the problem was Amazon was using proprietary data from its platform to push its own products. Small businesses can’t compete with that shit.

Recent revelations by Frances Haugen, the Facebook whistleblower, have only highlighted what we all know—that social media is terrible for most teens and kids. Social media platforms have long known this but had hidden the research and went about minting money while kids become nervous wrecks.

These are just a few of the most egregious and salient examples. Where there’s concentration, collusion, and cartelization becomes easy. Price rigging and cartelization are rampant across the world. In his must-read book The Myth of Capitalism, Jonathan Tepper put the cost of price increases from cartels at $600 billion, yes, a billion with a B.

There have several high-profile cases. As recently as September 2021, The Competition Commission of India (CCI) imposed a fine of ₹ 873 crore against United Breweries Limited, Carlsberg, All India Brewers Association (AIBA), and 11 others for cartelization. In 2016, the CCI had imposed a ₹ 6,715 crore fine against cement manufacturers for cartelization.

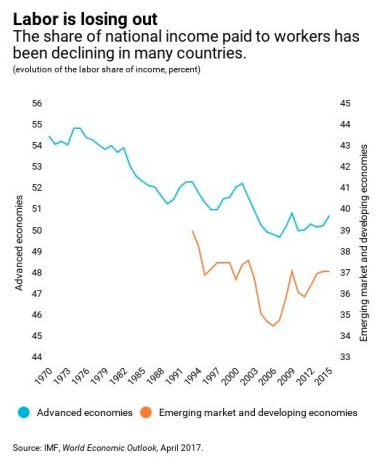

The problem with looking at things in the aggregate is that It’s hard to get people to care. Being the wisdomous person that I am, I call this the tyranny of aggregates. For decades, one of the big economic issues has been the rapidly falling share of labor across the world. Labor share is the percentage of national income that goes to workers in the form of wages.

Remember labor? Those poor 12-year-old kids that make your Nike sneakers you bought because you made a new year resolution to move your voluptuous ass away from your chair to slightly reduce its ginormous proportions? Those kids are called laborers!

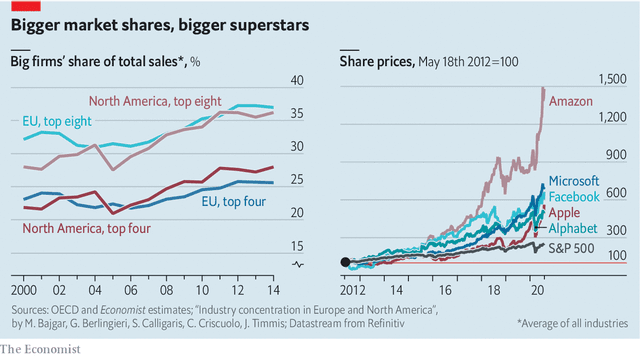

Labor share has been consistently declining across much of the world. Various economists have proposed various theories. On one side, you have people like David Autor who say that this is because of the “superstar firms” effect. Larger firms have become bigger because they are better at doing more with less labor, and hence a larger share of profits have accrued to them instead of labor.

This paper proposes and evaluates evidence for a new “superstar firm” explanation for the fall in the labor share of value-added. We hypothesize that markets have changed such that firms with superior quality, lower costs, or greater innovation reap disproportionate rewards relative to prior eras. We show that, consistent with a simple model, superstar firms have higher markups and a lower share of labor in sales and value-added. As superstar firms gain market share across a wide range of sectors, the aggregate (sector-wide) labor share falls.

Tech giants like Facebook, Google, Microsoft, and Apple are examples.

On the other hand, you have countless economists, legal scholars, organizations, and antitrust experts like Joseph Stiglitz, Matias Germán Gutiérrez, Jan Eeckhout, Thomas Philippon, Lina Khan, Sandeep Vaheesan, Jonathan Tepper, and Matt Stoller who argue that rising concentration is a result of lax antitrust enforcement, increased M&A, and regulatory capture among other reasons. This has resulted in a decreasing labor share because when markets are concentrated, the bargaining power of labor decreases because they can’t switch jobs easily.

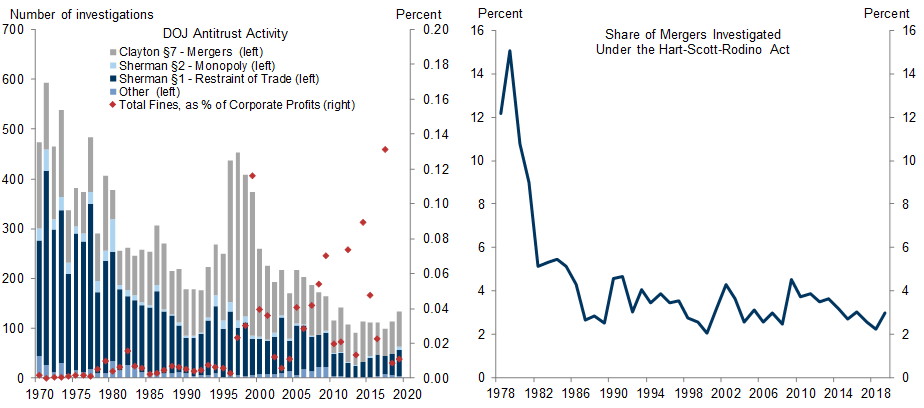

We can see this in the data. Antitrust enforcement cases have hit a record low:

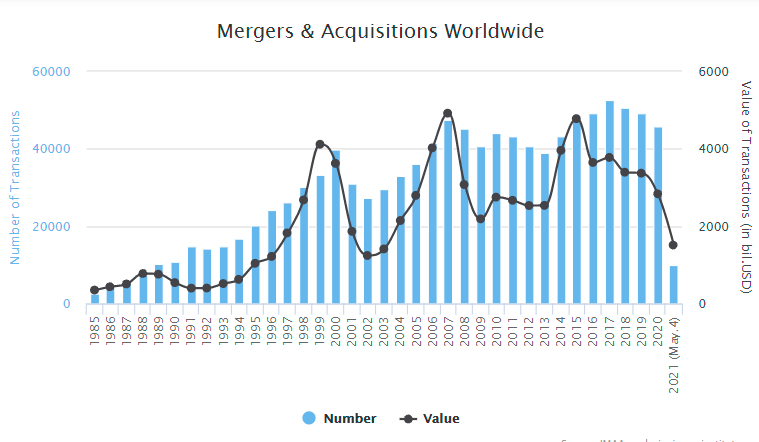

Falling antitrust and monopoly cases have coincided with a dramatic increase in M&A activity in the US, Europe and much of the world. Bigger companies have been acquiring smaller companies at a record pace:

Just the five largest tech giants have acquired over 616 companies like YouTube, Skype, LinkedIn, GitHub, Instagram, WhatsApp, and IMDB.

The FTC requires companies to report every acquisition worth more than $92 million. In a study released Wednesday, the FTC said Microsoft, Apple, Google, Facebook and Amazon together made 616 acquisitions from 2010 to 2019 that fell below that reporting threshold but were worth at least $1 million. Many of those acquisitions probably were never disclosed at all.

Washington Post

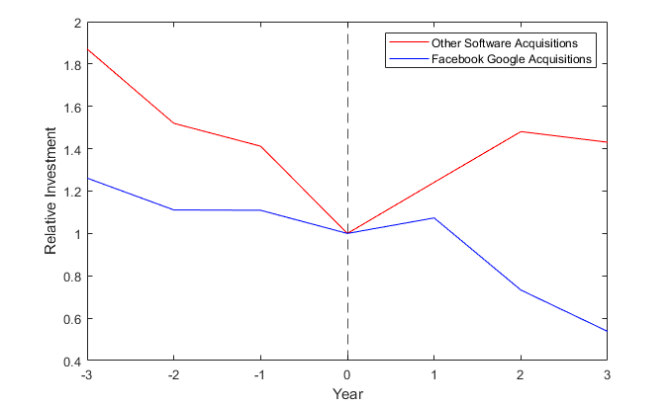

The most shocking paper I came across as I was writing was “Kill Zone“ by Sai Krishna Kamepalli, Raghuram Rajan & Luigi Zingales. Their research shows that Facebook and Google create kill zones—segments where VCs don’t want to invest—whenever they acquire a company.

Phenomenal. Their acquisitions cause VC investments in similar companies to drop sharply. That’s goddamn power!

There is no way in hell all these tech startups would be as powerful as they are today without acquiring all these companies. Given how hard it is to compete in the shadows of these tech giants, the startup rates have also decreased across industries.

This has created another perverse incentive. Xinxin Wang UCLA Anderson, in her research, found that entrepreneurs in concentrated markets build companies with the objective of getting acquired rather than to compete:

Her data, in a working paper, suggests that entrepreneurs entering these markets knowingly develop technology that aligns with the needs of major players, making their startups more natural acquisitions candidates. This is particularly true in concentrated markets where incumbent acquirers value innovation more because they can effectively appropriate the benefits of innovation and scale.

“Entrepreneurs cater to and engage in proximal innovations in order to present themselves as attractive acquisition targets, demonstrating the role that technological synergies play in acquisitions,” Wang says in the paper.

Catering Innovation: Entrepreneurship and the Acquisition Market

It's not just that; most of these mergers are useless, and anywhere between 70% to 90% of them fail. What's more, this whole consumer harm bullshit doesn't work either. Professor John Kwoka's analysis of FTC approved mergers found that in almost all cases they were a rise in prices.

We find that the antitrust agencies cleared the studied mergers about as often as they imposed remedies, although the percent cleared has risen over time. We further find that most transactions resulted in increases in prices post-merger, suggesting a permissive antitrust posture. The price increases were considerably greater for mergers subject to conduct remedies than divestitures, corroborating doubt about the efficacy of conduct approaches. Finally, we find that the agencies cleared mergers without substantial price effects systematically and significantly more often than mergers resulting in large price increases. This suggests that agencies have been able to distinguish, on average, case deserving of approval from those raising the most serious competitive concerns.

Does Merger Control Work? A Retrospective on U.S. Enforcement Actions and Merger Outcomes

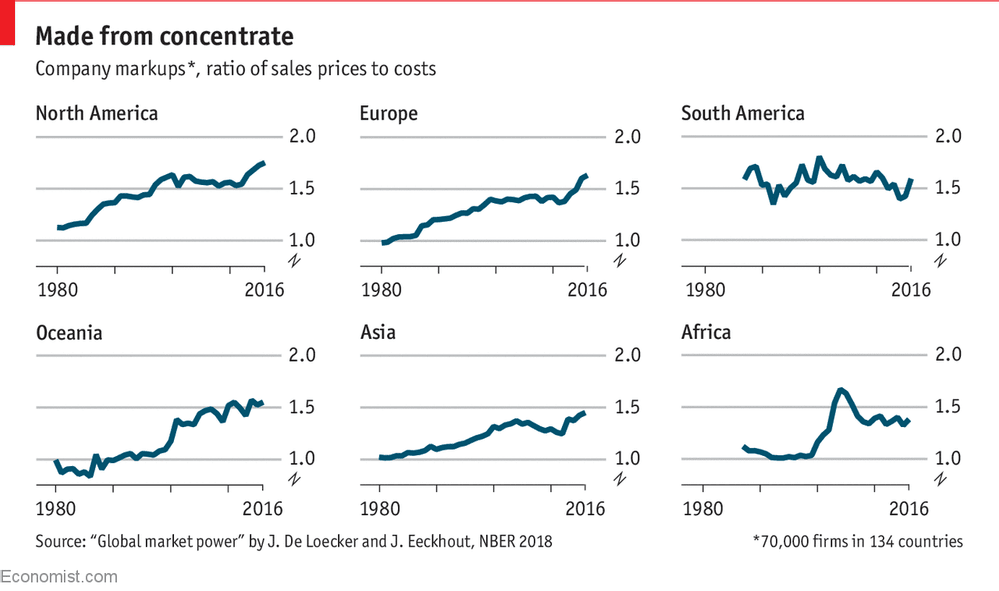

The side effects don’t just end here. A growing body of evidence shows that price markups—the difference between the cost of production and selling price—have been increasing for decades.

The researchers examine markups—selling prices divided by production costs. At 1, products are sold at cost; above 1, there is a gross profit. Using the financial statements of 70,000 firms in 134 countries, the authors find average markups rose from 1.1 in 1980 to 1.6 in 2016.

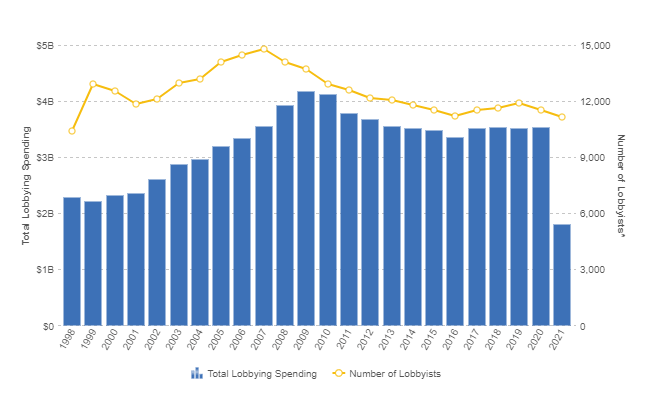

The other issue with the concentration of market power is the marriage of market and political power. We've seen this in the case of US banking and tech where there's a revolving door between regulators and ex-employees, it's not always bad, but it ain't good either. But the bad far outweighs the good. The poster child for shit going wrong is The Federal Trade Commission's decision not to sue Google despite overwhelming evidence that Google was anticompetitive.

Look at the growth in lobbying spending. Companies spent $3.5 billion (Rs 22,500 crores) on lobbying in 2020. Big tech companies were among the biggest spenders on lobbying:

So why is this all bad?

To answer this question, you need to know a bit about American antitrust history. I’m just going to focus on America in this post because it’s 25%+ of the global GDP and that’s where all of today’s largest companies operate.

Yes, knowing the past is important to be a successful income redistributor (scamster). The Amrikan history is littered with problems caused by large companies, monopolies and market concentration. This is a very reductionist version of history, but during the late 1800s, America faced a problem of large companies. The most famous example was Standard Oil, owned by John D. Rockefeller. Standard Oil used every illegal, unethical and anticompetitive trick in the book to crush its competitors. Standard Oil’s share of the petroleum industry went from 4% to 90% in the 1870s.

Around the same time, railroads were consolidating and were charging exorbitant freight rates. The farmers were pissed and started protesting. John Sherman was a senator from Utah, and he hated monopolies. He was pissed too and created a bill now famously called the Sherman Act, passed in 1890. The bill’s main goal was to ensure economic liberties, protection of small businesses, equal opportunities, and fair competition.

In enacting the Sherman, Clayton, and Federal Trade Commission Acts, Congress aimed to constrain corporate power broadly. The drafters of these landmark statutes sought to restrict corporate power over consumers, workers, suppliers, and rivals. And they also targeted corporate clout in the political system. Informed by republican ideology, they recognized that concentrated corporate power threatened the maintenance of democratic governance. Congress enacted the antitrust laws to protect consumers and sellers from the power of monopolies and trusts. As Robert Lande has detailed, the framers of the principal antitrust laws wanted to protect consumers from the tribute exacted by corporations with pricing power. Monopolistic and cartelistic prices were described as unjust wealth transfers and condemned as “robbery” and “theft.”

This was the same act under which Standard Oil was broken up into 34 separate companies.

The US antitrust movement was the strongest in the early 1900s. But by the 1970s, there was a dramatic change in the vision of antitrust. A bunch of lawyers and academics from Chicago managed to convince everyone that the primary goal of antitrust was consumer welfare and nothing else, in other words, economic efficiency above all else.

The Chicago school, built on the work of Aaron Director, an economist from the mid-20th century, reached its zenith in the writing of the legal scholars Robert Bork and Richard Posner. Its proponents argued that many activities which were assumed to be anti-competitive were entirely reasonable strategies for improving corporate efficiency. They also claimed that in some cases even things which couldn’t be justified that way could safely be left to the market to sort out without recourse to law.

The free markets would take care of other issues like market concentration, labor, and supplier exploitation. This was when the neoliberal movement started to take shape. Ronald Reagan comes to power in the 1980s, and he’s a real free markets believer. In fact, there’s a rumour that he once asked his wife Nancy to change her name to “Free Markets Reagen”. Margaret Thatcher was another notable free marketer of the time. It’s almost rumoured she had asked her husband if she changed her name to “Free Markets Thatcher” and some accounts show he fainted.

Starting in the 1970s, antitrust enforcement pretty much grinds to a halt. The Chicago school of thought becomes dominant—the belief that free markets will solve all the problems in the world, even erectile dysfunction, some people told me. But, by the late 2000s, there was growing evidence that this free market shit doesn’t work. Market concentration, income inequality, market power, coercive actions by monopoly like firms, and labor repression were rising, and competition, wages, startup and small business applications, investments, and market dynamism were all dropping off a cliff.

A new school of thought called The New Brandeis Movement, named after the famous Supreme Court justice Louis Brandeis—he hated big business with the passion of a Mexican Salsa Dancer—started becoming more vocal. The most popular face of this movement is Lina Khan, the current chairwoman of the Federal Trade Commission (FTC). She became famous for her phenomenally brilliant piece titled Amazon’s Antitrust Paradox. The crux of her argument was basically that the Chicago school’s neoliberal interpretation of antitrust sucked and was the reason Amazon and other tech companies had become so powerful, perpetrating abuses against workers and abusing their market dominance.

The movement was also derisively dubbed hipster antitrust by all the loyal free-market believers. The other notable faces of the movement are folks like Tim Wu, Matt Stoller, Sandeep Vaheesan, Jonathan Kanter, and Barry Lynn. This movement argues for a more nuanced and wider approach to the problem of market concentration, rather than a preoccupation with just consumer welfare like the Chicago boys. In a 2018 brief, Lina Khan outlined the core tenets of the movement like putting in structures that make it tough to abuse market power, refocusing antitrust on structures that lead to market power and abuse and away from a singular focus on consumer welfare, among others.

The Chicago boys, on one side, argue that unless prices rise and consumers are harmed, the regulators and antitrust laws shouldn’t bother about much else. They think that bigness is always a reward for the best companies, and bigness should be encouraged. They also think that the free markets will magically solve all the other problems if you rub your eyes three times and spit on the floor. On the other side, you have neo-Brandeisians who argue that just focussing on consumer welfare is what got us into this mess. This is why companies have grown so big, and if we don’t tackle these companies, they will engage in all sorts of shenanigans:

Focusing antitrust exclusively on consumer welfare is a mistake.176 For one, it betrays legislative intent, which makes clear that Congress passed antitrust laws to safeguard against excessive concentrations of economic power. This vision promotes a variety of aims, including the preservation of open markets, the protection of producers and consumers from monopoly abuse, and the dispersion of political177 and economic control.178 Secondly, focusing on consumer welfare disregards the host of other ways that excessive concentration can harm us—enabling firms to squeeze suppliers and producers, endangering system stability (for instance, by allowing companies to become too big to fail),179 or undermining media diversity,180 to name a few. Protecting this range of interests requires an approach to antitrust that focuses on the neutrality of the competitive process and the openness of market structures.

At this point, you have to a real fucking idiot if you think perfect competition works. I mean, you have to be on some really special kind of drugs and live in a weird perpetual trip, like an LSD semi-overdose, to be oblivious to the corrosive and sinister effects of market concentration and power. The largest companies have been happily running various sophisticated income redistribution schemes to steal from everyone while distracting you by giving you free apps that allow you to broadcast your narcissism to the world —selfies, pouty face, vacuum ass or whatever the hell is trending right now.

Having said that, just big isn’t bad. That’s one thing both the Chicago boys and the Brandeisians agree on. Certain companies tend to become natural monopolies.

One reason natural monopolies occur is, as Fiona Scott Morton, another leading voice in the antitrust movements, points out, human behaviour. The tendency of humans to exhibit herding, preference for defaults, information anchoring mean that they will never truly explore all products as is rationally expected of them. Some firms are better than others at exploiting these human biases to defend their market dominance. And there’s nobody as good at behaviour hacking as the big tech companies.

The Brandeisians argue, and rightfully so, that you need to have regulations that structurally make it difficult for big firms to engage in shenanigans like suppressing wages, killing competition, erecting entry barriers, mistreating suppliers and so on.

Having said that, enforcing antitrust is profoundly difficult, and things are incredibly subjective. What a company might deem to be normal without malice and ill-intent can be perfectly construed as being anticompetitive. Because antitrust doesn't work in perfect isolation, where harms are measured against the benefits, it's inherently political. There are also a lot of conflicting agendas competing at any time. Will antitrust action lead to the US finding it difficult to compete against China? Will it fall behind in the race for patents? Will antitrust action kill national champions? Will I piss off big chemical companies and tobacco companies, who are my biggest political donors?

Sandeep Vaheesans sums it up best:

Antitrust regulates state-enabled markets, which cannot be separated from politics. The history of antitrust law shows competing visions of both the law’s aims and its methods, suggesting there is no “apolitical,” universal concept of antitrust. Rather than aspire for an impossible utopia of “apolitical” antitrust, we must decide who should determine the political content of the field—democratically-elected representatives or unelected executive branch officials and judges.

The Twilight of the Technocrats’ Monopoly on Antitrust?

I think antitrust will be among the most important issues of our time, and it’s an inherently political issue, meaning it’s subject to pissing contests and dick-measuring contests. Just in the last five years, the amount of noise in this debate, particularly against big companies, is more than in the last 20 years. Antitrust was in a blissful coma, nobody cared about it, and the Chicago boys were ready to pull the plug. The Chicago/free-market school of thought had won.

But the antitrust and anti-big sentiment is getting quite serious, alongside rising populism and the disenchantment with income inequality. The Europeans and the US both now have people who hate monopolies in positions of power. Margrethe Vestager, the top antitrust enforcer of Europe, has imposed 3 of the biggest fines totalling nearly $10 billion against tech giants—Google in this case—in the last 4-5 years for anticompetitive practices. Lina Khan rose to fame because of her antimonopoly stance now heads the FTC. Not just that, The United States Department of Justice (DOJ) and several states have active investigations and cases against tech giants.

Things are quite similar here at home in India. The Indian government has repeatedly chastised Amazon for its anticompetive practices. The RBI has grown queasy about the concentration of UPI marketshare between just Google Pay and PhonePe and wants to issue a new payments license. India also introduced data localization laws. This is in line with the "big is bad"sentiment sweeping the world. But antitrust actions require nuance. The loudest view often tends to be about how big is unequivocally bad, and it's stupid. I have a feeling such loud views and political posturing will lead to a lot of really really stupid choices and decisions by our fossil politicians and ossified bureaucrats in the years to come.

Just curtailing size can have serious counterintuitive effects on innovation which inevitably feeds back to the consumers in the form of higher prices. This is the same argument that the neoliberals like Joshua Wright of George Mason and the former FTC commissioner and The Information Technology and Innovation Foundation (ITIF), which is funded by tech companies have made.

While I was researching this damn thing, I couldn't help just how fractious this debate is. Even among the left so to speak, there's a severe disagreement between the moderates and the radicals.

Given the enormous stakes, I wonder how this shit pans out.

Further reading

This topic is incredibly fascinating and fun, at least for me. I came across some amazing perspectives and people, and I've become a fan of some of them like Fiona Scott Morton, for example. So here are a few links if you want to go deeper down this rabbit hole:

Sanjukta Paul. I can't recommend her work enough, and it is a must-read if you want, what is perhaps the most unique take on antitrust law. Her framing of antitrust as an allocation of economic coordination rights is bloody genius. MUST-READ!!!!! Her LPE articles are an easy and less intensive read.

Fiona Scott Morton: More Profits and Less Antitrust Enforcement

Shit you won’t read, and I won’t stop sharing

I’ve been increasingly thinking about these links. Not many people click on them, I think this information overload is the culprit here and I’m just making it worse and I know it. So, I’ve been thinking of how to solve this, one idea I’m toying with is summarizing all these things in a short post with TLDR like snippets and all the interesting things. I don’t know if that’s the answer but I think it’s worth a shot. If you have any other ideas, leave a comment or twat at me.

Personal finance and investing

Multibagger stocks aren’t rare, but that doesn’t mean it is easy to find them

When Financial Intermediaries Sneeze, These Assets Catch a Cold

Thought provoking article

Very informative, thanks for sharing