The right way to do active management

The right way to do active management

The active management edition

This edition was delayed because #HairTwitter was trending on Twitter.

In one of the previous issues, we talked about how China, the world’s largest 100% pure democracy, is in the midst of a very measured and subtle crackdown against some of its biggest finance, education, and tech companies.

A recap of the subtle interventions so far:

Ant IPO was scuttled. Alibaba was fined $2.8 billion and Jack Ma was forced to step down as chairman

JD, Meituan, Baidu, Pinduodo were all hit with fines

Didi Chuxing's apps were taken down from app stores and the Cyberspace Administration of China (CAC) launched an investigation

Tencent, Baidu, Bytedance, Alibaba among others were hit with fresh fines last week. Tencent is expected to face new lawsuits

The CCP ordered school tutoring companies to become non-profits.

The regulators called online gaming 'spiritual opium". An attack on gaming companies like Tencent is coming

Reports suggest other sectors like healthcare, real estate etc are in the crosshairs of regulators

State govt firms were ordered to migrate data to cloud services run by the government. They can no longer use private cloud providers like Alibaba

The crackdown is so subtle that The Communist Party of China’s (CCP) took a baseball bat to the knees of several companies. The hits have left several of these companies like Didi, Tencent, Alibaba begging for mercy. In the same issue, I wrote about how the best way to understand The Communist Party of China’s (CCP) motivations is to think of it like the mafia.

The CCP mafia craves control above all else. If you are operating under the patronage of the mafia, you can do whatever you want, as long as that’s within the boundaries set by the mafia. The moment you step on the boundaries, you’ll be subject to some broken kneecaps and facial bones.

But there’s another lens we need to look at this from. The CCP mafia is an active fund manager.

Now, the job of an active fund manager is to generate alpha, i.e., beat a chosen benchmark. There are various ways to do this. They can generate outperformance by identifying undervalued stocks. They can also do insider trading by finding drunkards in public companies, getting them drunk and disclose non-public information. I had even written a step by step guide to successful insider trading. If you’re an active manager and are reading this, you’re welcome!

Or they can be activist investors. Find companies that aren't living up to their potential, buy decent stakes, get some board seats and start agitating for change. Selling business divisions, mergers, acquisitions, firing the CEOs and so on.

The CCP mafia is a brilliant activist investor. Now, the CCP makes two types of investments in its companies - financial and reputational. It makes financial investments and acquires stakes, and takes board seats in promising startups. Just last week, the CCF mafia acquired a 1% stake in Bytedance, the parent company of Tik-Tok and Weibo, the Chinese version of Twitter.

Through state-owned enterprises and funds like the China Internet Investment Fund (CIIF), the CCP mafia owns stakes in several companies like Kingsoft, Kuaishou, Ximalaya, Tingyun, Full Truck Alliance, Sensitime, and Cloudwalk, among others. It’s even considering taking stakes and board seats in Alibaba, Tencent, and Chinese media companies.

Apart from financial investments, it also has reputational investments. Given that the CCP mafia craves control Above all else, it can’t afford these companies trying to overshadow or work with its enemies.

Now, if you’re an activist investor in undemocratic dictatorships like the USA and European countries, you need to follow the law of the land. You need to get board seats, apply pressure on the management to make changes, fight boardroom battles, file lawsuits, engage in courtroom battles, media fights, etc. It’s tiresome.

But the CCP mafia controls China, which is a democracy on steroids. It doesn’t need to do stupid things like following the rules, respecting the law, etc. That’s what amateur active managers do.

Take the case of Ant Group. A private equity fund run by the Ant Group had made investments in a few companies controlled by a CCP mafia party secretary who was arrested on Corruption charges. The CCP mafia stopped the IPO, fined the company, launched several investigations, and deposed Jack Ma, the Ant and Alibaba group chairman. That’s the advantage of democracy.

Now, the CCP mafia has a diverse portfolio. Several of these companies have done phenomenally well. But they were doing things like listing in enemy territories like the USA, anti-competitive practices, price gouging, which led to the people becoming unhappy, among other things. This is strictly not ok in a super democracy like China.

If people become unhappy due to the actions of these companies, there will start protesting, which might lead to revolutions. Then the CCP mafia has to divest (kill) thousands of people, which is a media nightmare. These are issues that are a threat to the legitimacy of the CCP mafia. So the CCP mafia finally sent its capos to break some noses and knee caps.

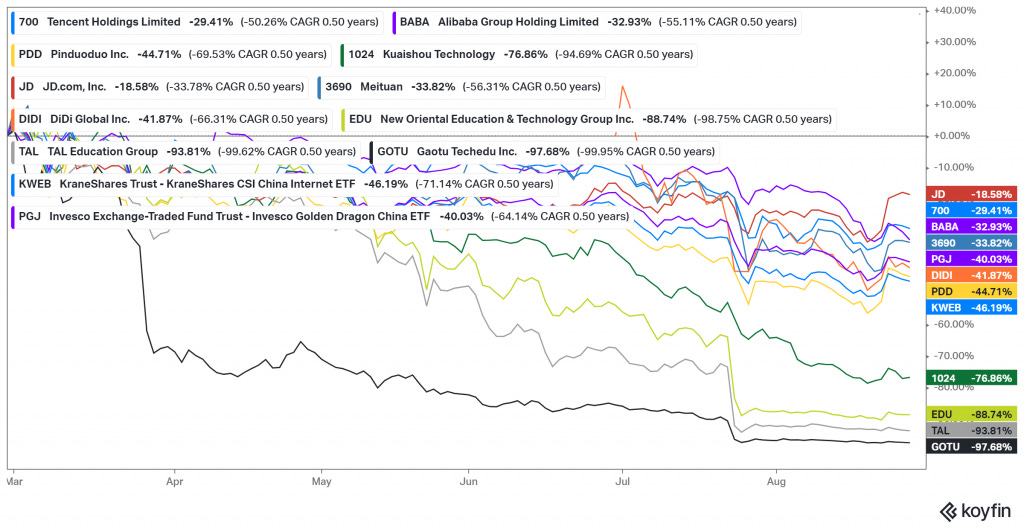

Now, in the short run, there might be pain. Some of the biggest Chinese stocks have taken it on the chin in the last couple of months:

But in the long run, once the companies feel the pain, say sorry 100 times and buy the CCP mafia some cookies, they’ll let you off the hook and let you do whatever you want. This means the CCP mafia’s PR problem goes away, and the companies start growing back again, which means the CCP’s holdings value increases too. Two birds, one baseball bat. This is how you do active fund management.

You don’t do stupid things like ask the management nicely to do the right things to increase profitability and share price. You take a baseball bat, crack some knees and force them to beg you to do the things you want them to do anyways.

So, the moral of the story. If you are an active fund manager, you should threaten to break the legs of the CEOs of the companies you hold.

Bullet behind the back

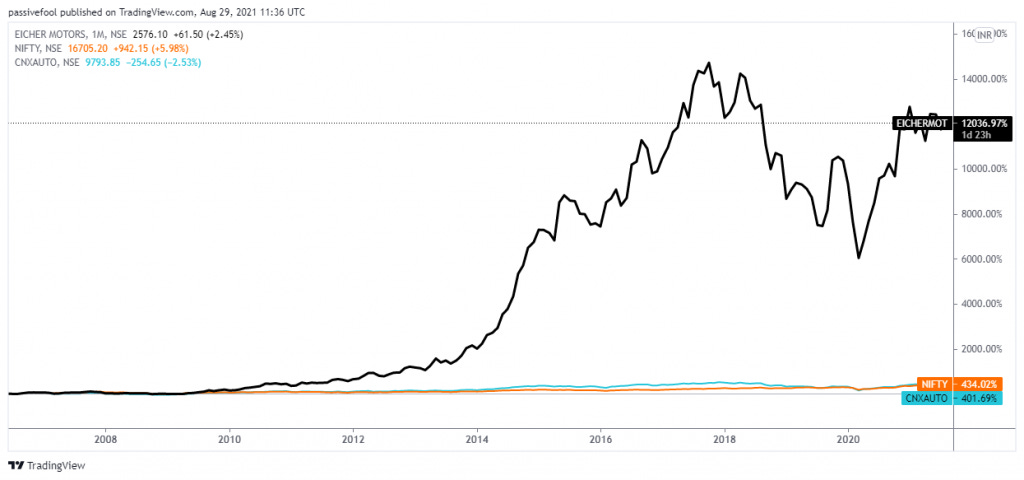

There was a fair bit of drama last week over the reappointment of Siddhartha Lal as the Managing Director of Eicher Motors. Siddhartha Lal was largely responsible for the stunning turnaround of the middling Eicher Group back in 2006, and the company has done well since.

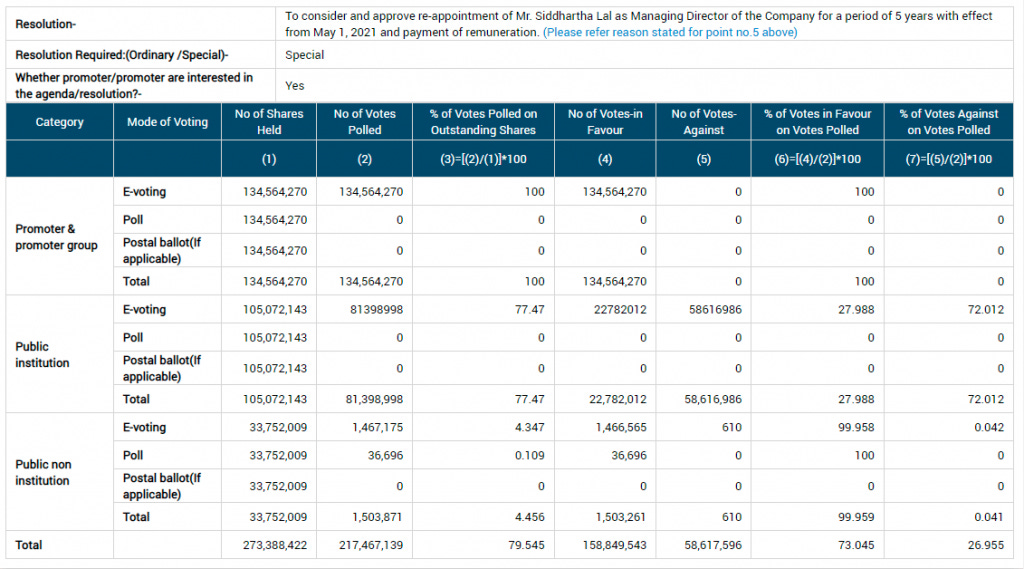

In the AGM last week, the proposal to reappoint Siddhartha Lal and increase his remuneration failed to get the requisite majority of 75% votes. The proposal failed because institutional shareholders such as mutual funds voted against a salary hike for Mr Lal.

Now, here’s the thing. Institutional shareholders like mutual funds, insurance companies and public pensions have grown quite big over a period of time. Public companies must seek shareholder consent for key issues like board appointments, compensation schemes, mergers, buybacks etc. Typically, retail investors don’t really care about these things and don’t vote. It’s mostly the promoters and institutions that vote.

Now, institutional shareholders like mutual funds hold shares of 100s of companies. In the case of a fund like the Vanguard Total Stock Market Index Fund, it holds shares of 3935 companies. Except for large asset managers, smaller asset managers and indexing-focused asset managers can’t afford to have in-house resources to analyse each shareholder proposal and then vote.

So, entities called proxy advisors started to fill this need. These firms specialize in analysing shareholder proposals and offering recommendations to shareholders on how to vote. They sell this as a product to asset managers. In a way, proxy advisors are like credit rating agencies. In the US, just two firms – Institutional Shareholder Services Inc. (ISS) and Glass, Lewis & Co. (Glass Lewis) account for 90% of the proxy advisory market. In India, Institutional Investor Advisory Services (IiAS), InGovern and Stakeholder Empowerment Services (SES) are 100% of the market.

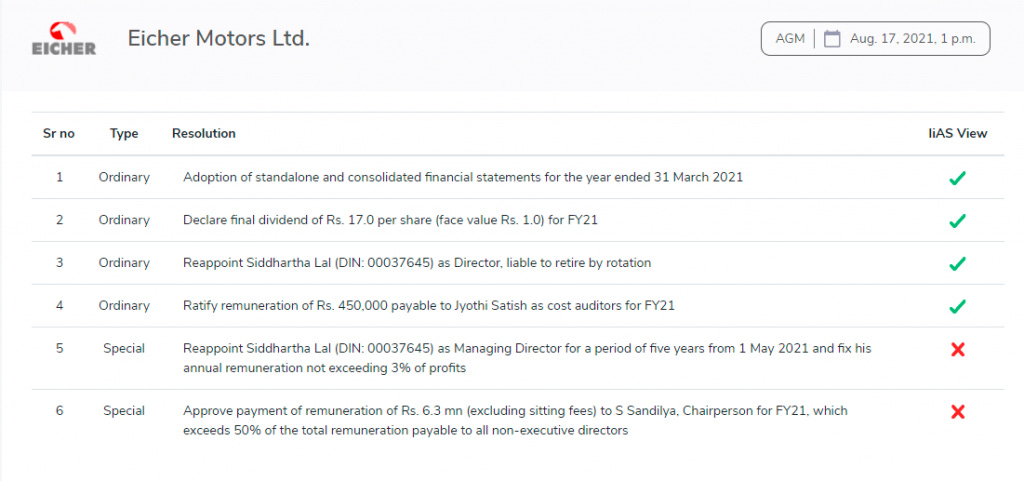

Now, given that most institutions don’t have the resources to analyse shareholder proposals, they mostly end up voting in line with the management or based on the proxy advisors’ recommendations. It was the case with Eicher as well. Here’s the recommendation of IiAS:

The institutions voted on the recommendation of IiAS, and the proposal was rejected. He was later reappointed after Eicher revised the pay package for Mr Lal to a maximum of 1.5% of the profits:

Speaking about the outcome of the Annual General Meeting and specifically about the remuneration issue, Mr. S Sandilya, Chairman of Eicher Motors Ltd said, “The Nomination and Remuneration Committee (NRC) of the Company has considered all the factors, including inputs from various stakeholders including institutional investors before recommending remuneration for key managerial persons. The primary concern with investors was not Siddhartha’s reappointment as Managing Director or the proposed compensation; it was the lack of clarity regarding the enabling provision that potentially allowed payment of remuneration upto 3% of profits.

Over the last four years, we have had the same limit of 3%, but in reality have paid only a fraction of that amount. The actual remuneration during FY2021 was at 1.04% of profits, with the preceding years being at a lower percentage” Given the background of actual remuneration paid to the Managing Director in preceding years, the Board has now approved a revised remuneration structure for the Managing Director, with a maximum cap of 1.5% of profits as per Section 198 of the Companies Act. Specific details of the remuneration are being shared via the postal ballot.

Now, I don’t really have any view on whether Mr Lal deserves the package or not. You can argue both ways. But what bothers me is the power that proxy advisors like IiAS are wielding. This isn’t just an Indian issue but rather a global issue. The scale of these proxies is quite stunning:

Institutional Shareholder Services (ISS). ISS is the largest proxy advisory firm in the United States and globally. Founded in 1985, ISS is based in Rockville, Md., and maintains offices in 13 countries. The firm employs approximately 1,000 individuals, serves 1,700 institutional clients, and provides proxy recommendations on 40,000 shareholder meetings in 117 countries. It is owned by Genstar, a private equity firm.

Glass Lewis & Co. Glass Lewis is the second largest proxy advisory firm in the U.S. and globally. Founded in 2003, the company is headquartered in San Francisco, Ca. It employs 1,200 people and provides voting recommendations on 20,000 shareholder meetings in 100 countries. It is jointly owned by two Canadian pension funds: Ontario Teachers’ Pension Plan and Alberta Investment Management Corporation.

Milken Institute even had published a report that said that the rise of proxy advisors is a market failure. Over the past decade, the influence of these proxies has come under increasing scrutiny. This is because of the growing dominance of institutional shareholders and the rise of passive focussed asset managers. Given that asset managers, particularly passive focussed ones, can’t afford to analyse every proposal, they became the biggest customers of proxies.

And by their very definition, passive focussed asset managers like Vanguard don’t really meddle with the management. 90%+ of the time, they vote in line with the management and based on the recommendations of proxies. This behaviour led to the term “robo-voting“. Whether this is right or wrong is a separate argument and one that I don’t want to get into. This has led to a debate over whether passive focussed asset managers like Vanguard, Schwab etc., should adopt a more active stance when it comes to shareholder voting. This is often used as a strawman’s argument to say that index funds are destroying capitalism. It’s a stupid argument, but that’s a rant for another day.

And the regulators are aware of this issue. The U.S. Securities and Exchange Commission (SEC) issued new guidelines to curtail their influence last year, and so did SEBI.

Now, there are two things that bother me here.

One

These proxies are far too influential. Judging by the above states, it’s easy to assume that proxies are evil. They aren’t. They fill a huge void in the market.

Proxy advisory firms have no choice but to be rule based, in coming up with internally consistent recommendations across thousands of proposals. To their credit, they view rules as guidelines with some flexibility. They incorporate idiosyncratic considerations and invest time in understanding management rationale behind specific proposals. However, across dozens of resolutions from hundreds of companies, discretion is limited. On balance, they (rightly) err on side of being rule-based. Across thousands of proposals they provided voting recommendations for, they likely got it right over 95% of the time. That’s way better than most processes in messy world, including ours. However, any rule-based method will occasionally shoot down reasonable proposals, like the one we started with. While this trade-off can be minimized, it can never be eliminated. Universal laws governing type-1 and type-2 errors are inviolable.

But that doesn’t take away the fact that they are prone to conflicts of interest, opaqueness and vote capture. For example, Institutional Investor Advisory Services India Limited (IiAS) shareholders include Aditya Birla and UTI mutual funds, Axis Bank, ICICI Bank, and Fitch Group. IiAS makes voting recommendations on and to these companies. The other issue is that these firms are almost monopolies or oligopolies. This leads to other issues that can potentially have an impact on market efficiency:

The fact that the proxy advisor sets its fee strategically, aiming to maximize its own proÖts rather than the informativeness of voting, creates an ineffeciency of another sort. In our model, when the advisorís information is imprecise, firm value would be maximized if the advisorís recommendations were made prohibitively costly, so as to maximize shareholders incentives to perform independent research. In contrast, when the advisorís information is su¢ ciently precise, firm value would be maximized if the price of the advisorís recommendations were made as low as possible. Clearly, neither of these policies is optimal from the monopolistic advisorís perspective. When the advisorís information is imprecise, it charges low fees to induce shareholders to buy its recommendations. This crowds out independent research and leads to overreliance on the advisorís recommendations. In contrast, when the advisorís information is very precise, this information is underused: to maximize profits, the monopolistic advisor rations information, selling it to only a fraction of investors. Interestingly, because of this strategic pricing, informativeness of voting does not increase even if the advisorís information is perfectly precise, as long as the cost of private information acquisition is not very high

But this will remain a thorny issue with no or difficult solutions.

Two

Should active managers be making these company-specific judgements? I get that that’s their job. But given that 70-80% of active managers don’t beat their chosen benchmarks, which is their only job, what makes them qualified to tell how other companies should run their business? If 70%+ of them can’t generate 10bps of alpha over the benchmark to justify their salaries, what makes them qualified to say that Mr Siddhartha Lal’s salary is high? How would they even know they’ve never justified their salaries. Forget salaries; they’ve never justified the value of all the dry fruits they get for free during Diwali.

This reminds me of David Graeber’s Bullshit Jobs theory.

A bullshit job is one that even the person doing it secretly believes need not, or should not, exist.

If my own research is anything to go by, bullshit jobs concentrate not so much in services as in clerical, administrative, managerial, and supervisory roles. A lot of workers in middle management, PR, human resources, a lot of brand managers, creative vice presidents, financial consultants, compliance workers, feel their jobs are pointless, but also a lot of people in fields like corporate law or telemarketing.

If there was ever a job that belongs at the top of the bullshit jobs, it would be active management. I’m not saying all active management, just to be clear. Most active management, i.e., closet indexing masquerading as “high conviction” stock picking, is a net negative to society. These are leeches slowly bleeding unsuspecting investors dry by charging high fees while gathering assets.

Active management is the ultimate bullshit job of all, even worse than a McKinsey consultant.

The committee to save the world

Now, there's another problem here. You know, for supposedly being the smartest creatures in the universe, we humans do some profoundly dumb shit. For decades we knew that burning shit meant that we are ruining the planet. But no, we decided not to stop burning shit and instead distracted the world by giving the Kardashians a TV series and Kangana Ranaut a Twitter account while we happily kept burning more stuff and kept ruining the planet.

Now that we've realized, we're all going to die because of all the burning, saving the world has become a mild priority. Now, where there are priorities, there are opportunities for income redistribution (scams). Enter Environmental, Social, and Governance (ESG) investing. After making investors rich by robbing investors blind by charging high fees and deliver shit performance, active managers have somehow managed to convince enough people that they can save the world just by picking stocks. Yep, you can save the world just by investing in an ESG fund.

Meanwhile, the moronic scientists and policymakers are wasting time and money trying to find scientific solutions🤦♀️. The audacity of these idiots when they could've bought some stocks and saved the world. For most parts, ESG is a bloody scam. It's an income redistribution scheme (scam) designed to transfer money from gullible investors to the pockets of useless active managers.

Now, for better or worse, active managers have a part to play in our desperate attempt to save the planet from climate change, having ruined it by incessantly farting and releasing toxic gases while watching Keeping Up with the Kardashians. Companies affect the environment and since active fund managers have voting rights in the companies, they have a role to play in steering companies not to fuck up the planet any more than they already have. The same goes for proxy managers, since most fund managers blindly mimic their voting recommendations, their decisions can directly impact the fate of the world - no exaggeration.

Now, if an active fund manager can't justify his salary and do his job of beating a benchmark even if his life depended on it, should we trust them to save the planet from melting? This is a bit like giving an 8-year-old kid a box of crackers and matchsticks and expecting him to do the right thing i.e., not to burst the crackers.

I mean, a bullshit job like active management has a say in saving the world. God help us. If I were you, I wouldn't dare hope that we're going to make it. We're going to die and the best thing you can do is start a SIP.

Things that can make you smart

Investing and personal finance

Your formative experiences have a strong bearing on how you invest

It’s always better to focus on the process of your retirement planning than on abstract numbers and percentages. The false sense of security from precise numbers is a recipe for disaster

Just remember, the stock market can crash quite a bit

The best way to be unhappy in life is to compare yourself to others, especially about how much money you have

You can never be too careful when being specific, especially when its about stocks

Brain stuff

Tech & work

Critics vs Haters, Or, Why The World Needs More Real Criticism

What I learned visiting two cutting-edge Amazon grocery stores

The Pro-Office “Silent Majority” Is A Lie, And The Powerful Want Remote Work To End

Crypto

Afghanistan

Econ stuff